We are only two months into 2026, and markets already feel chaotic.

Gold surged and then crashed.

Bitcoin rallied and then sold off.

Software stocks ripped higher before pulling back hard.

Investors are anxious.

Is the gold bull market over?

Will Bitcoin recover?

Are stocks too expensive to buy now?

When markets feel confusing, the best move is not to panic. It is to zoom out.

Let’s step back and answer three critical questions:

- Where are we in the economic cycle?

- How will this cycle drive asset prices?

- Where are the real opportunities in 2026?

Since the US dollar remains the anchor of global assets, we begin with the US economy while comparing other major regions.

The Global Recovery Is Gaining Momentum

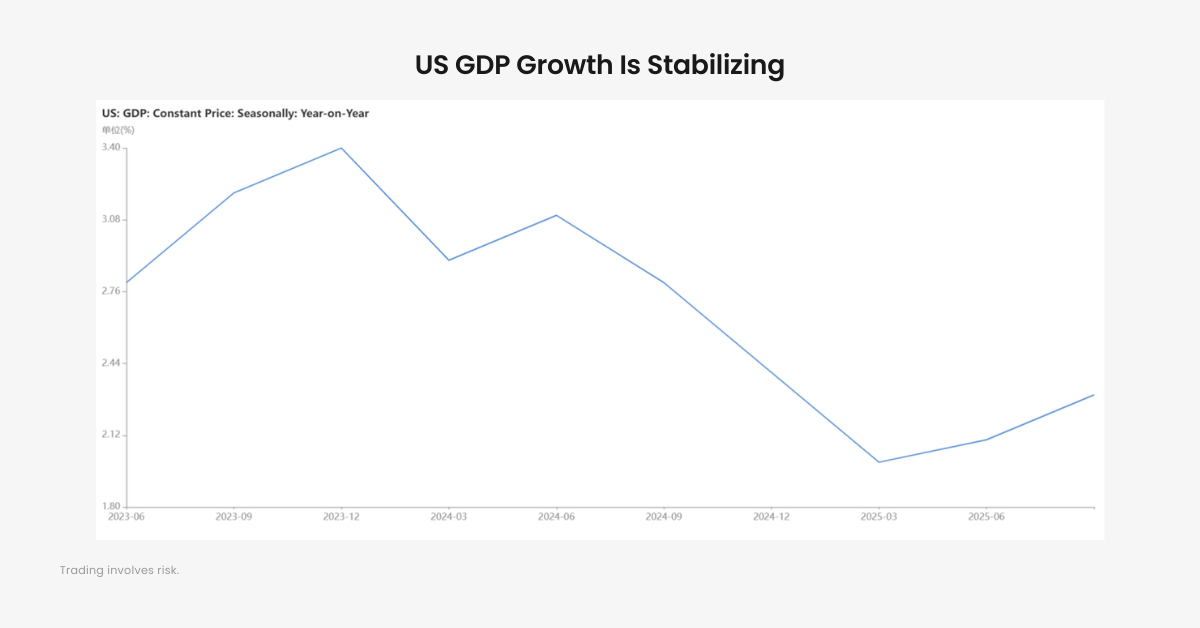

After a sluggish 2025, the US economy is showing renewed strength.

The latest GDP data is still pending, but leading indicators point to recovery.

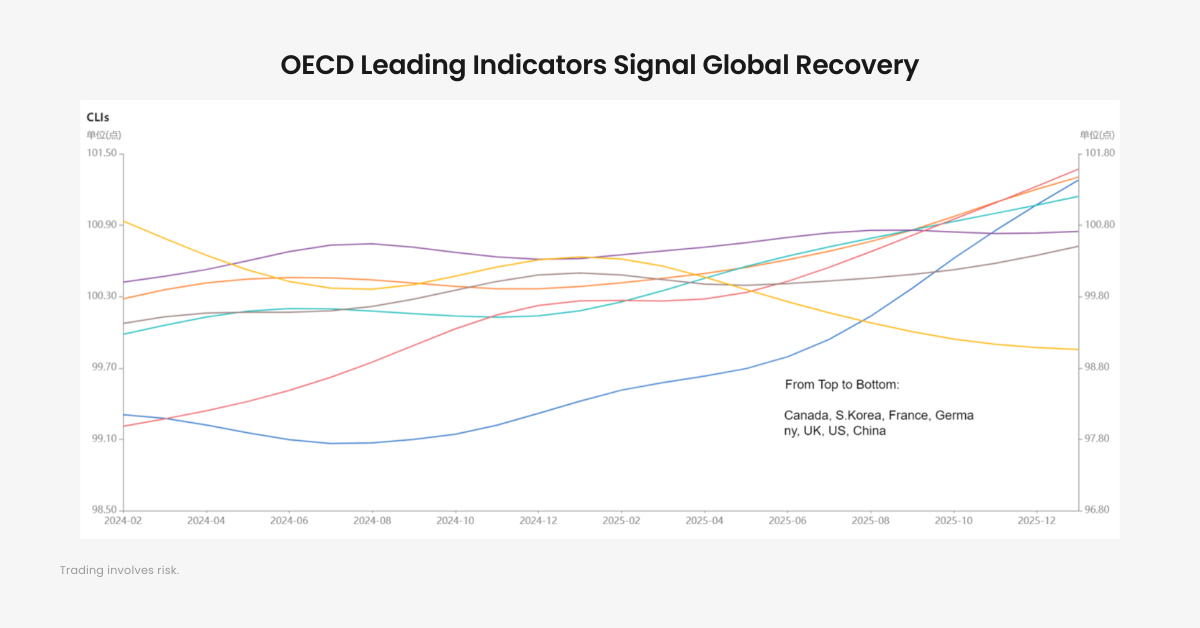

The OECD Composite Leading Indicator for the US rose to 100.55 in January 2026, up from 100.42 the previous month. While that may seem small, leading indicators turning upward signal momentum building beneath the surface.

Hourly wages increased 3.76 percent year over year in December 2025, up from 3.62 percent in November. Since consumption drives nearly 70 percent of US GDP, wage growth is critical.

In short, the US economy is stabilizing and improving.

The Recovery Is Not Just American

The OECD system of Composite Leading Indicators (CLIs) for Canada, South Korea, Germany, the UK, and France have also been trending higher since 2025. The Eurozone, in particular, appears to be gaining strength.

However, China remains the exception. Its leading indicators are still trending downward, reflecting an ongoing structural transition.

PMI Data Confirms the Expansion

Purchasing Managers’ Index data provides another layer of confirmation.

In the US:

- ISM Manufacturing PMI rose to 52.6, well above the contraction threshold of 50

- Markit Manufacturing PMI increased to 52.4

Both readings signal expansion.

Germany’s ZEW Economic Sentiment index jumped to 59.6, showing strong forward expectations.

Japan’s PMI stands at 51.5, also in expansion territory.

China’s PMI, however, remains at 49.3, below 50, indicating contraction.

The pattern is consistent. The US and Europe are entering a recovery phase. China is still working through structural headwinds.

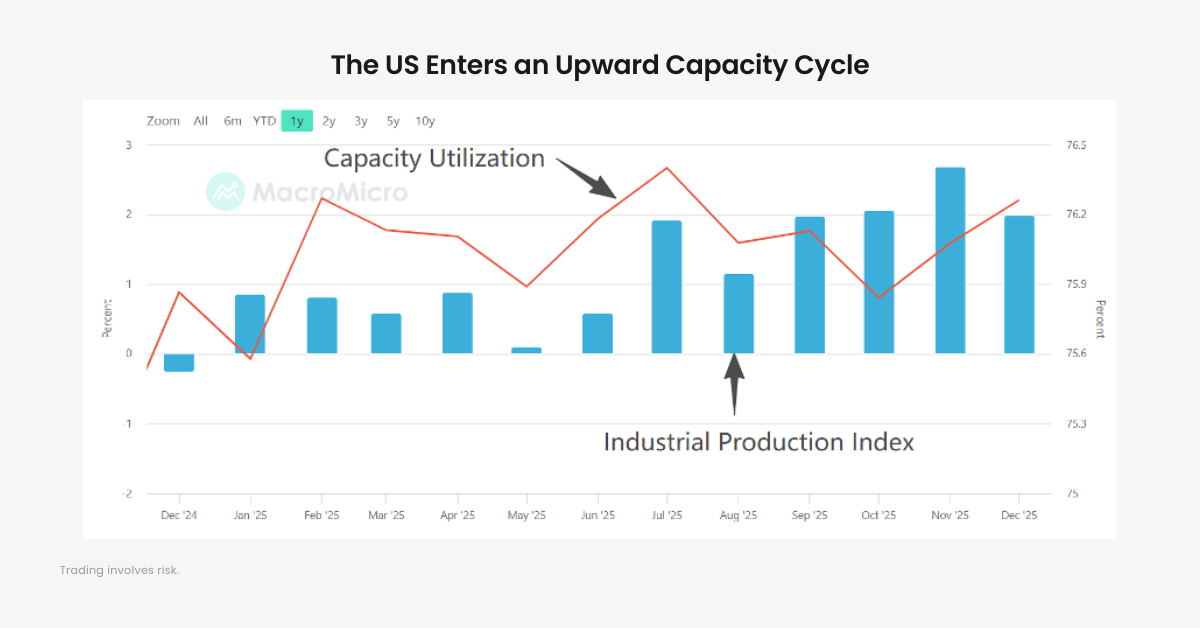

The AI Capacity Cycle Is Beginning

US capacity utilization and industrial production are both rising. This suggests we are entering a new phase of the Juglar cycle, also known as the capacity cycle.

What is driving this cycle?

Artificial intelligence.

Massive investment in AI infrastructure, data centers, and computing power is fueling industrial expansion. This is not just a hype wave. It is capital expenditure translating into real economic activity.

Technology is no longer just a market theme. It is becoming the backbone of this recovery.

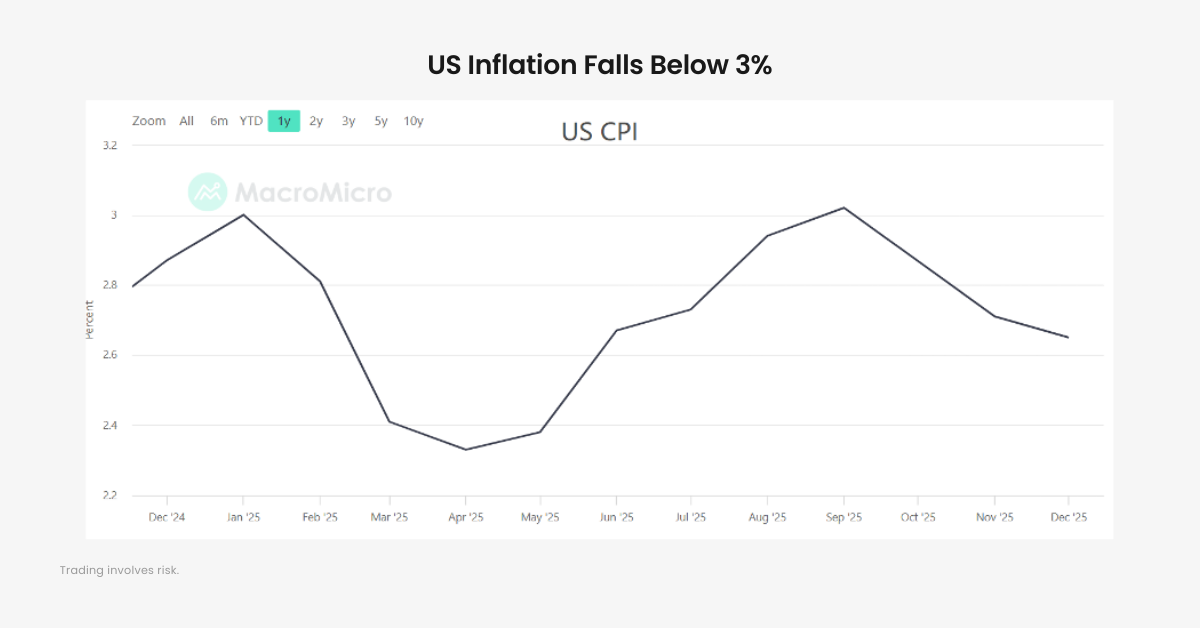

Inflation Is Under Control

After peaking near 9 percent during the pandemic era, US inflation has cooled significantly.

CPI briefly moved above 3 percent in late 2025 but has since moderated.

The Federal Reserve has managed to reduce inflation without triggering a deep recession. That is a difficult balancing act, and so far, it has worked.

However, this creates a paradox.

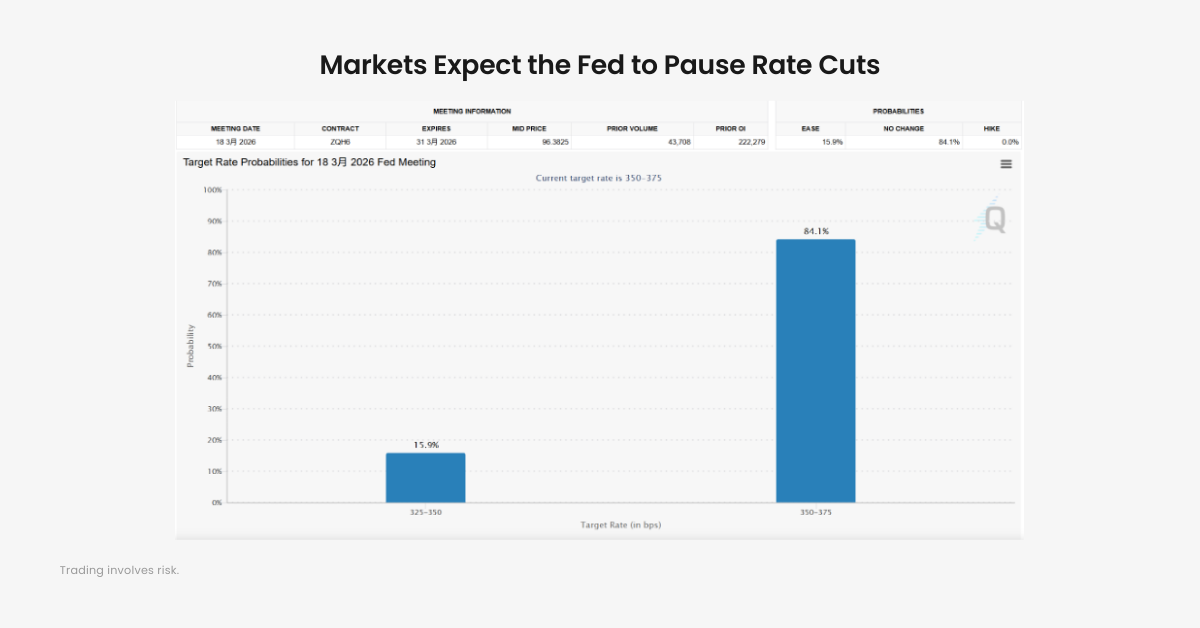

Strong economic data means the Fed does not need to cut rates.

According to CME FedWatch data, markets currently assign an 84 percent probability that rates will remain unchanged in March.

This is why markets are nervous.

In 2026, good economic news can temporarily pressure risk assets because it reduces the urgency for rate cuts.

Kevin Warsh and Liquidity Concerns

Kevin Warsh, expected to lead the Federal Reserve, has indicated support for balance sheet reduction.

If the economy remains strong and inflation reaccelerates, tightening liquidity becomes possible.

Shrinking the balance sheet increases real Treasury yields. Higher real yields raise the opportunity cost of holding non-yielding assets like gold and can pressure speculative assets such as cryptocurrencies and high-growth stocks.

Liquidity, not just growth, is now the market’s central focus.

China’s Transition Is Still In Progress

While the US is managing inflation, China is dealing with deflationary pressure.

China’s CPI turned positive after September 2025, suggesting deflation may be stabilizing.

However, the real estate sector remains weak. The cumulative year-over-year growth of floor space sold continues to decline. Property has not recovered and is still searching for a bottom.

China is pivoting toward technology sectors including solar energy, electric vehicles, and AI manufacturing. This transition shows promise, but structural shifts take time.

In the first half of 2026, housing-related sectors such as appliances and construction materials are unlikely to outperform.

Where Is the Opportunity in 2026?

Despite media narratives focused on risk, the data tells a more constructive story.

The US economy is expanding.

Europe is improving.

China is stabilizing but restructuring.

Inflation is moderate.

The stagflation fears that dominated headlines are fading.

So why are stocks, gold, and Bitcoin pulling back?

The answer is liquidity expectations.

Markets are adjusting to the idea that rate cuts may be delayed and balance sheet reduction may continue. A short-term pullback in risk assets is logical in that environment.

But a pullback does not equal a collapse.

The Best Bet in a Recovery Cycle

D Prime believes equities remain the strongest opportunity during a recovery cycle.

In the short term, the Nasdaq may experience volatility due to tighter liquidity conditions. However, strong companies continue to grow earnings when economic activity improves.

Over time, earnings growth drives stock prices higher.

Investors should expect short-term fluctuations but remain patient. Recovery cycles reward disciplined capital, not emotional trading.

Final Thoughts

Markets feel unstable because they are adjusting to new policy expectations.

But beneath the volatility, the global recovery is building momentum.

Economic cycles drive asset prices. Liquidity shapes timing. Earnings determine long-term direction.

In 2026, the bigger picture matters more than the daily headline.

The question is not whether markets will move.

The question is whether you are positioned for the cycle we are entering.

Risk Disclosure

Trading in Securities, Futures, contracts for difference (CFDs) and other financial products carries high risks due to the rapid and unpredictable fluctuation in the value and prices of these financial instruments. This unpredictability is due to the adverse and unpredictable market movements, geopolitical events, economic data releases, and other unforeseen circumstances. You may sustain substantial losses including losses exceeding your initial investment within a short period of time.

You are strongly advised to fully understand the nature and inherent risks of trading with the respective financial instrument before engaging in any transactions with us. When you engage in transactions with D Prime, you acknowledge that you are aware of and accept these risks.

Disclaimer

This article may contain speculative statements regarding future expectations, plans, or projections based on information and assumptions currently available to D Prime. Although D Prime considers these assumptions reasonable, such statements involve risks, uncertainties, and factors beyond D Prime’s control, and actual outcomes may differ significantly.

This information contained in this blog is for general informational and educational purposes only and should not be considered as financial, investment, legal, tax or any other form of professional advice, recommendation, an offer, or an invitation to buy or sell any financial instruments. The content herein, including but not limited to data, analyses and market commentary, is presented based on internal records and/or publicly available information and may be subject to change or revision at anytime without notice and it does not consider any specific recipient’s investment objectives or financial situation. Past performance references are not reliable indicators of future performance and D Prime and its affiliates give no assurance that any views, projections, or forecasts will materialize.

D Prime and its affiliates make no representations or warranties about the accuracy or completeness or reliability of this information and disclaim any and all liability for any direct, indirect, incidental, consequential, or other losses or damages arising out of or in connection with the use of or reliance on any information contained in this article. The above information should not be used or considered as the basis for any trading decisions or as an invitation to engage in any transaction. Do not rely on this report to replace your independent judgment. You should conduct your own research and consult with an independent qualified financial advisor or professional before making any financial trading or investment decisions.

“D Prime” is a brand name of D Prime Vanuatu Limited, a company incorporated and regulated by the Vanuatu Financial Services Commission (Company Number: 700238). The availability of products and services may vary depending on jurisdiction and applicable regulatory requirements.