Good morning.. Yet again we saw a strong and late rally on Wall St on Friday and it seems that a lot of the days action comes at the end of the day and it is rarely negative. This has had the impact of creating another strong weekly close for US stocks. This may have implications for the USD after a strong sell-off. My point is that towards the end of the week, EU stocks under-performed and the USD rallied, suggesting that capital inflow may have stalled or reversed. I will be interested to see how EU stocks hold up against the US this week and right from the off we have a lot of data to deal with.. This will be a busy week. Also the steep and aggressive rally in USDJPY was suspicious to say the least and there is talk that an “official hand” was behind the move or they got someone to do their dirty work for them. But this turned the USD and we saw an extension last night to 106.40. This has done a lot of damage to the charts for USDJPY and indeed many JPY crosses (very clever). European, UK and US PMI manufacturing today but final looks for some. Caixin PMI was strong but will the demand be there for Chinese goods? Right now, I think unemployment, the consumer and global trade are key points to focus on and none look positive.

Keep the Faith..

Details 03/08/20

How can global growth recover until a vaccine is found? A big week ahead:

–

Cases of the virus across the globe are rising and rising rather fast as we scramble to find a vaccine, get is passed the regulators and out to where it is desperately needed and until we do, there has to be a very real danger that the global economy will suffer. The knock-on effect from a lack of footfall in major cities, the psychological impact on the consumer and falling demand, suggests that company earnings are looking rather bleak for most. The ripple effect from so many still working from home is large, as so many businesses rely heavily on the likes of London, NY, Paris and Tokyo, thriving and bustling with workers spending money. The tourist and hospitality businesses are in tatters and look like they will remain so for quite some time. People have either chosen not to travel or have been unable to do so and the economic impact on this is simply vast, as the effects will reverberate through nearly every industry and business, from manufacturing to real estate, restaurants, luxury goods, financial services; you name it.

All this will risk setting off a raft of corporate insolvencies, high unemployment and a sharp downturn, much of which is still to be seen. The issue here is that the insolvency issue may not be priced and we still seem to have quite a disconnect between the economic outlook and equity prices. The crisis is widespread and global. Even with billions of dollars in government aid programmes, US commercial bankruptcies were up 43 per cent in June compared with the same month of 2019. It is hard to imagine what will happen when the bailouts stop coming. On that note, we still await an agreement from the US government on replacing the benefits for those unemployed through no fault of their own. Time is running out and it looks likely that there may be a gap now until further funds reach those that need it in time. Unemployment and the consumer are at the heart of everything, along of course with any vaccine success and related headlines will be seized upon and this week, we not only get US weekly jobless claims but Non-farm payrolls data which will have picked up the rise in claims over the last 2 weeks. People are not eating out and in the US, the decline in manufacturing jobs over the past two decades was matched by a rise in food service employment (cheap labour burger flippers), but that increase has now gone into sharp reverse.

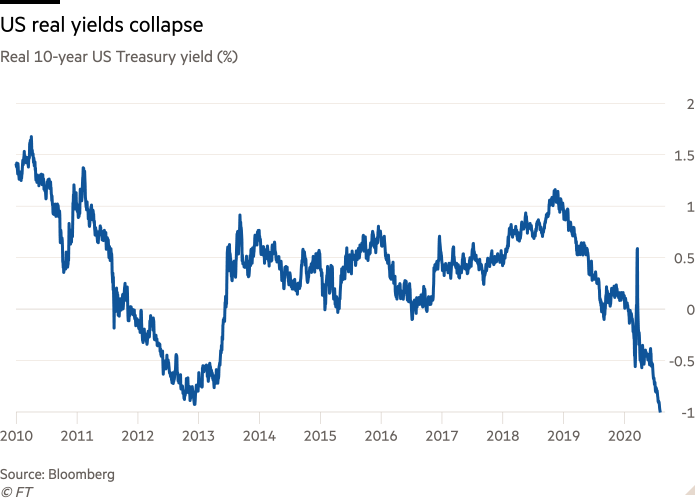

Cities are like ghost towns and holidays are being taken at home which has a massive impact on so many associated businesses and many will not survive and many may not have a job to go back to. This is not confined to the US; this is on a global scale. We still have a lot of hope that we can see an end to all this and many are looking to China for clues as to how a recovery can take hold. Last night, the Caixin PMI showed the biggest improvement in operating conditions in China’s manufacturing sector in almost a decade. But they had a draconian lockdown which many western governments are not prepared to go back to and demand for Chinese goods may yet be slow to recover and have an impact down the road. I am not sure that China is a template for us all on that basis and looking at US and many other bond markets, bond investors are not buying into it either. Yields across the US curve are hitting all-time lows and Real yields on US Treasuries hit minus 1 per cent on Friday, reflecting investors’ readiness to pay up for safe assets as a surge in coronavirus cases threatened the country’s nascent economic recovery.

Line chart of Real 10-year US Treasury yield (%) showing US real yields collapse

The situation in the US is NOT improving; in fact it seems to be getting worse and there is not the slightest hint from the Fed that rates will be moving up anytime soon. In fact, if we listen to central bankers around the world, there is a similar thread of fear in what they see ahead. We will hear from the RBA and the BoE this week. Markets do not price a hike in US rates until 2023. What will happen to global growth between now and then? On top of this, we have started phase2 of the trade war between the US and China and others are getting dragged into it. I am sorry but the outlook seems rather bleak and I am an optimist!

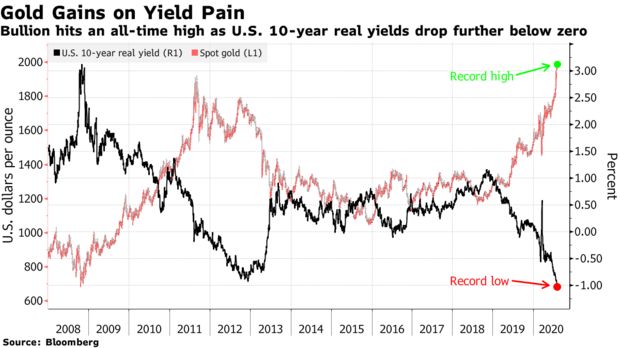

Bullion hits an all-time high as U.S. 10-year real yields drop further below zero

Central banks may try some more policy moves but their impact on the real economy is over and they know it. It is now all down to governments to bite the bullet and spend like crazy to get us through this. That, of course, comes with side-effects but with rates so low it seems most will be happy to take the plunge and a plunge it is, as we are stealing from the future and our children will not thank us for this.

I have said for a while that the data would recover quickly after economies were pushed into a forced coma and then unlocked but a V-shaped recovery in data was no indication of a V-shaped recovery for the economy and high-frequency data is starting to suggest that things are topping out again. With a lot of the problems stemming from the US economy, it does question whether the USD may keep falling as there is a possibility that the USD becomes the vehicle to express US weakness rather than selling stocks, which have clearly benefitted from Fed stimuli. Along with unemployment data in the US, we also see figures on motor sales, manufacturing activity, construction spending and consumer credit, which offer further clues on whether the recovery remains on track; it’s a big week. But Q2 nominal consumer spending declined at an annualized rate of 35.8%. But the actual decline is much worse. BEA estimated that people’s rent payments in Q2 increased $ 2 billion to a record $641 billion. But BEA methodology assumes people made their rent payments on time and in full, yet, reports show that more than one-third of renters skipped paying part or all of their rent in Q2.

We are not in normal times but some things still make one look twice. Q2 in the US saw a record decline in Nominal Output and a record increase in financial (equity) wealth. Based on preliminary data the market capitalisation of domestic companies increased by $7 trillion in Q2 while nominal GDP, measured quarterly, declined by approximately $500 billion. Here is a visual of that:

That divergence is not normal. To put some colour on this, the ratio of the market capitalisation to Nominal GDP stood at 2x times at the end of Q2, surpassing the prior record high of 1.87x times at the end of the tech bubble in Q1 2000.

Global trade is at the heart of how we get back to some kind of normality and for that to recover we need a vaccine. The danger here is that the US stance on China sees global trade suffer; just when we need it most. President Xi Jinping reiterated his recent call for “dual circulation,” emphasising self-sufficiency in supply and demand. The combination of a weak global economy and anti-China sentiment in the West, means China has to rely more on itself. Can the world afford to have China start looking inward? We already know that they are keen to move to a more service-based economy but if they are looking to be more self-sufficient as well, the implications could be hugely damaging to global trade.

China will substitute some imports, including technology, with local supply, and reorient some exports to domestic markets. In other words, global trade, which is already contracting, is likely to remain sluggish due to Xi’s pivot inward. This isn’t good news for countries that sell to China, including Germany, Australia and most emerging markets.

The recent USD move demands some attention but there may be a couple of signs that the sell-off is slowing and looking at EU equity underperformance into the end of last week, it suggests that capital flow into the EU may have stalled. The USD bounce looks like it may have been more than just month end demand.

Also the steep and aggressive rally in USDJPY was suspicious to say the least and there is talk that an “official hand” was behind the move or they got someone to do their dirty work for them. But this turned the USD and we saw an extension last night to 106.40. This has done a lot of damage to the charts for USDJPY and indeed many JPY crosses. My stop is close so I will leave it there for now but USDJPY looks a different picture now. I am not sure if this USD bounce across the board is virus related or not and certainly the high-frequency data in the US has not been that great but EU PMIs today may hold a clue. Markets are starting to suggest they expect more from the Fed which to be honest is a USD negative but the feeling is that the US government simply has to find a compromise on the bail-out programme to replace those that expired Friday. This may be USD supportive but I think that any rally, possibly overdue, may be short-lived due to the impact of high unemployment in the US lasting longer than many think. The Fed is NOT going to stop debasing the USD so a rally may be a great opportunity but Covid cases rising in Europe is a concern and anywhere where we see more lockdowns is likely to see the currency hit. On that basis, keep an eye on the UK and Oz as well.

The pandemic crisis is unique in that it involves public health, finance, and the economy. An all-out policy/rescue package pushed finance and the economy far ahead of the public health crisis. Unfortunately, the public health crisis lives on and is eating into the heart of most economies again. So the rebound in finance and the partial recovery in employment are fragile at best and will take a lot longer than originally thought to pass. I am not sure that all the cost-cutting and staff layoffs has taken place yet! In the US, they simply have too much retail space and consumers have been forced to embrace online shopping and realise how easy it is and how well it works. There is going to be a massive reset in the US retail space and closures look a certainty and jobs will be shed by the boatload. Bankruptcies are yet to hit but they are coming. But it is not just the US economy which is weak, the outlook for the global economy, with a lack of demand for those recovering to sell to, continuing job losses and trade wars, suggests that many assets, having raced ahead on hopes of a recovery, may need a reset.

—————————————————————————————————————-

Strategy:

Macro:.

Short USDJPY @ 105.25.. Stop at 106.75

Long EURAUD @ 1.6250 stop at 1.6080

Brought to you by Maurice Pomery, Strategic Alpha Limited.

—————————————————————————————————————-

Strategic Alpha Report Disclaimer

Doo Prime endeavor to ensure the reality, adequacy, reliability and accuracy of all the information provided, but do not guarantee its accuracy and reliability. All the information, analyses, comments, statements, and/or data provided in this report is for information purposes only. Client’s use of any contents of the report as the basis for the transaction, the client shall fully aware of the risks and agreed to bear all the risks. Client shall cautiously judge the accuracy of the information. Doo Prime has no liability for any loss caused by any inaccuracy or omissions of the contents and subjective reasons of Client.

Risk Warning

This information is powered by Strategic Alpha. Any opinions, news, research, analyses, prices, other information, or links to third-party sites are provided as general market commentary and do not constitute investment advice.