Good morning.. So, that is March and month end behind us and stocks immediately take a dive, which I have been expecting and for too long they have ignored damaging virus stats from Europe and mostly in the US. Trump finally admits the scientists might be right!! I think we are entering phase5 of this sell-off and it could be ugly with either a test and bounce from the recent lows or a deeper capitulation and low set. My fear it is the latter and we have had a huge stimulus already. This brings the question of the USD move now and it’s a tough call in a rout, as that usually sees a push into US bonds and thus a bid for the USD. But is this time different with the fact that the Fed is so active in bonds and rates are where they are now? The swap lines the Fed has in place has alleviated a lot of USD demand. Would cash be the only alternative for now? With that in mind I am booking the profit in Cable and selling EURGBP up here on this bounce to .9000 area. I still think the EU is facing a crisis moment. The euphoria seen in stocks recently, lured many back in but this phase looks like an ugly one to me but for those with dry powder, opportunities will emerge. I remain bearish the S&P but admit I was a day early. Strap yourselves in.

Keep the Faith..

Details 01/04/20

Month end now behind us; can stocks hold? Phase 5 begins! Switching from Cable to EURGBP.

–

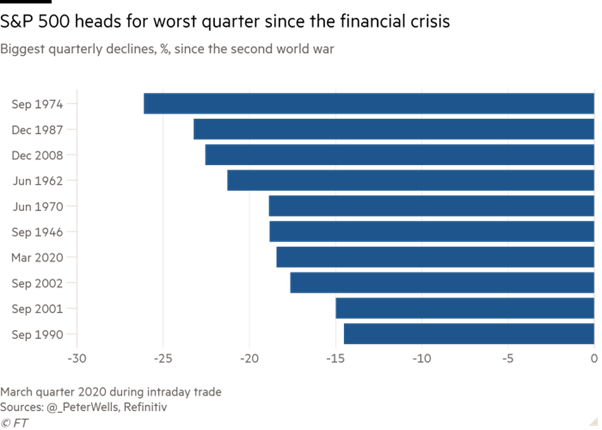

Global equities have had a bad quarter and that is putting it mildly. US stocks were on track for their biggest quarterly drop since the financial crisis on Tuesday as they wobbled between positive and negative territory in their final trading session of the period.

It was a nervous affair with the added stress from the 4pm Fix for currencies but that is all behind us now and the question is where now? It was a worrying close and I fear we are entering phase 5 now of the sell-off where we either test recent lows and bounce creating the mother of all double bottoms, or we see further deep capitulation and make new lower lows. My fear is the latter as the hope and euphoria has dragged a lot of investors back into buying. We saw the initial shock from the spread of the virus (phase1) and then the realisation that dips will not hold (phase2) and a low was set. Then we saw the actions from the Fed slashing rates (phase3) and stocks started to rise. Then we saw massive fiscal stimulus programmes from the central banks (phase4) and the rally extended. Now we have seen the euphoria dashed as the virus keeps infecting and the delay to any recovery is noted and stocks may tumble again (phase5). For me it is now just about where the sell-off stops. This could get ugly.

The issue is that some serious props have now been removed from the equity markets as buybacks are banned or postponed and the pension fund rebalancing is done (and it was huge). The reality is that markets seemed to be ignoring some pretty dreadful stats still emanating from Europe and indeed the US. I just wonder if stocks can hold now as the good news seems to be missing still.

Even if peak virus is seen globally (which it isn’t yet), the period after is going to see businesses struggle to get back on their feet and attain full capacity and I am not sure all the unemployed will walk straight back into jobs. Plus the data is about to start catching the shutdowns and some nasty shocks are on the way. French, German and EU manufacturing data are seen this morning but all are final looks of previous data and we get a look at UK this morning which again is a final read with US ISM this afternoon after the ADP private sector employment data. ADP will be interesting as it covers most of March.

For the US, though, a new forecast for gross domestic product published by Goldman Sachs suggested a 34 per cent annualised contraction in the second quarter, indicating it is still to see the worst of the crisis. The bank is now predicting a US unemployment rate of 15 per cent by mid-year. Many analysts are coming out with similar scary headlines and the data will be bad; we know that. Some say it is priced but no way! How does that sit with equity investors and earnings forecasts? It looks pretty bleak but I guess we know this is coming but the issue is still how long the damage lasts. To my mind, this is not looking like a V-shaped recovery. This bear market has been unusual, not because of the scale of the decline but rather because of the speed and the volatility. I fear some of the euphoria may now wear off. Is all the expected bad news priced? I am not sure it is after this impressive bounce off the lows. Fear may again dominate greed. I would like to have dry powder to take the opportunity to get some investments at stressed levels and I remain bearish the S&P even though I was a day early with the call (apologies for that). With another fall coming after all the stimuli from CBs and governments, what more will/can they to do to stop the rout?

Meanwhile we saw new recent lows in EURGBP yesterday. With the cross trading as low as .8810 at one point. I still fell that the rallies will be sold into until the EU sorts itself out and starts acting as a Union and I recommend taking advantage of this rally to .9000 area and I have suggested a short here at .8901 and will take profits on the Cable trade here at 1.2380. The playing field needs flattening out and Germany, the core of the Union itself, has to step up if this union is to prosper as one. I don’t see that happening until something really ugly happens; if at all. Eurobonds are a great idea in theory. European countries would have access to funds to boost spending and lower taxes without increasing their national debt. The problem is that it is seen by the wealthier nations as a wealth transfer mechanism and Germany is afraid (correctly) of being bled dry to save the less disciplined peripheral nations like Italy and Spain. No Eurobonds and no banking union probably equals no EU in the long run and the group are being severely tested right now on their commitment to this project and rather than step up to the plate for the union, Germany and the Netherlands are taking a step back. Says a lot about the foundations of this union when it is in trouble. The repercussions will come via a shift in politics as populist governments will be forced by angry voters to demand more from the EU or leave. This is a crisis in the making.

The wealthy nations suggest there is the ESM to turn to but that has flaws. Using the ESM raises a political issue, as the ESM can grant loans only on the basis of an adjustment program agreed with the European institutions, which contains a series of conditions. Resorting to the ESM thus creates a stigma. It may signal a fragility to the markets and a relative loss of sovereignty with respect to the strings attached. Rather unfair during a crisis but it is what it is. The issue here is that Italy and others are seriously piling up debt. Maybe the Italians and Spanish should get together and say we’re going to issue 20% of GDP in debt in the next 3 months and then see what happens; call their bluff. I am not saying Italy or Spain would be better off outside of the EU but Italy has been in recession just about since it joined while Germany, France, the Netherlands and others have prospered; massively. The wealth divide within the EU is as damaging as it is in society anywhere and ends up with social unrest and political change. THAT is coming to the EU soon and the ECB cannot fix the politics.

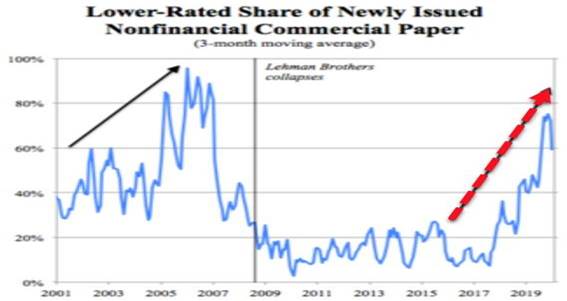

There is no doubt that the Fed has gone all in and surpassed even what it was previously allowed to do but many companies, in fact, now look more vulnerable to financing shortfalls than in the run-up to the 2008 financial crisis. The issue here is that the Fed safety net is going to support the higher rated companies when some of the real stress is with those not rated so preferably. U.S. manufacturing firms’ short-term liabilities have been climbing steeply since 2009 and it is clear that most are relying more and more on commercial paper to meet short-term liabilities. As the chart below shows, large shares of nonfinancial commercial paper issued since 2017 have come from lower-rated companies—much like in the run-up to 2008. Plus, many restaurants and small businesses will never reopen.

All this suggests that Fed buying will not stem the rising tide in corporate defaults and default a few of them may. I am sorry but I think equity markets may still have a sting in the tail. I think they will recover; but not from here.

The Fed did extend its swap lines to foreign central banks (i.e. foreign central banks will be allowed to exchange Treasuries held in custody at the Fed for US dollars) and to me this is another reason to sell the USD as the funding stress and USD demand should now ease and I still see this USD lower, especially as any month end distortions are over. In fact the USD sell-off may surprise a few but there will be some confusion as in a rout in risk assets, the USD usually does well. But has the Fed intervention in the markets changed that? I guess the question being what else do you buy? The Fed is making massive commitments here, many of which are unprecedented and of questionable legality. But it is clearly needed and they have eased some pressure but the Fed cannot stop the economy cratering if businesses cannot open. But more help is on its way apparently as the White House and Congress are already planning the next phase of fiscal stimulus even before the current one hits anybody’s pockets. It appears help is on the way for the mortgage market, as mortgage firms complain the Fed’s action is wiping them out, for the travel industry, and for states and local governments. Some of that will be bailouts and some of it might even be actual economic stimulus, with the total package being talked about in the range of USD600bn. Once upon a time that was a lot of money.

The US is about the only place that could get away with this debt issue that is building and even they may find it tough with all the debt issuance coming. That is going to make calling the USD from here pretty tough. But let’s see how OZ, NZ, Canada and the UK, ultimately fare as they go the zero rates and unlimited QE route as if there is natural market demand for them globally; and emerging markets are in a far deeper hole if they want to push back fiscally against the ‘rules of the game’ in the same way that developed economies are. There could be some massive consequences for all this. Can G20 and G10 survive when currencies really start flying around. A lower USD will help the global economy but many will be very unhappy with rising local currencies. Currency war anyone? So, is a lower USD or a higher USD what we need? Will there till be the rush to US bond markets for safety with rates down here and the Fed so active? Maybe cash is a better option for now and that means repatriation. USDJPY and USDCHF look high to me.

—————————————————————————————————————-

Strategy:

Macro:.

Long Cable at 1.1675.. Taking profits this morning @ 1.2380

Short EURGBP today @ 8901.. Stop above 9020.

Short S&P 2558

Brought to you by Maurice Pomery, Strategic Alpha Limited.

—————————————————————————————————————-

Strategic Alpha Report Disclaimer

Doo Prime endeavor to ensure the reality, adequacy, reliability and accuracy of all the information provided, but do not guarantee its accuracy and reliability. All the information, analyses, comments, statements, and/or data provided in this report is for information purposes only. Client’s use of any contents of the report as the basis for the transaction, the client shall fully aware of the risks and agreed to bear all the risks. Client shall cautiously judge the accuracy of the information. Doo Prime has no liability for any loss caused by any inaccuracy or omissions of the contents and subjective reasons of Client.