Good morning.. Japan was closed but a mixed session in Asia after a muted response on Wall St to better US NFP data. Interestingly the better data saw the tech sector underperform with the NASDAQ down almost 1%. The USD remains rather more of a two-way bet now after the technical picture shifted on Fridays close with the likes of the EUR posting a weekly “Doji” suggesting a momentum stall to the recent move. I think the outlook for the USD is more clouded now and I have made some tweaks (see below) to the positions. But I still feel the Fed is at the heart of USD weakness and they may be back in USTs starting to soak up all the issuance again soon. Some consolidation is expected but the fundamentals are little changed for me despite the data. I am getting very worried about how far the WH will go in prodding China as the health Sec. lands in Taiwan. This is a red line for China and this demands attention. Better data on the inflation front from China and US JOLTS data may be interesting later. I think this is a big week for the USD..

Keep the Faith..

Details 10/08/20

The USD rallies as US data suggests an early emergence from the crisis.

–

The headline NFPs beat expectations and after some stronger than expected data during the week in the likes of ISM data, the USD had a serious bout of profit taking on Friday as questions arose about the speed of the US recovery against other major nations. Trump said it was going to be a good number and it was (is it legal for him to comment on market sensitive data before release? It shouldn’t be allowed.) The BLS reported that in the end the good news was that the US economy added 1.763MM, which while above the 1.48 million estimates, was still well below June’s record 4.8MM surge. But as the ADP payrolls report hinted, the manufacturing sector is starting to sputter, with just 26K jobs added in July. Putting the rebound in context, the US economy still has a way to go before it fills even half the labour gap that opened after the March Covid shutdowns

I think we are seeing the knee-jerk reaction to unlocking of the economy and reopening of businesses who are taking back furloughed staff but as is the case elsewhere, especially the UK it seems, those jobs may be far from safe as firms start to cut costs aggressively.

The unemployment rate also continued to slide and from 11.1% last month it declined to just 10.2% in July, well below the 10.6% expected. Curiously, almost the entire gain in payrolls was the result of a shrinkage in the number of “temporary unemployed” which dropped by 1.34mln to 9.225mln. This needs some attention. The question is: at what point do all these millions in “temporary layoffs” become permanent? The issue for me is that US firms receive the government assistance if they take these staff back but they do not have to hold onto them. In the UK for example, one in three U.K. employers plans to cut staff this quarter, highlighting the growing risk of a labour market crisis derailing the post-lockdown recovery as government support is withdrawn. The same will apply to the US and cost cutting looks to be the next unemployment issue building. Also the Democrats and Republicans have failed to reach an agreement on the continued support package for unemployed workers and Trump has had to partly intervene with an executive order which will see the support cut from $600 a week to $400.

The two sides are as far apart as they ever were on agreeing how best to tackle this issue and in the meantime, millions are getting extremely concerned about their welfare. Trump also ordered a suspension of the payroll tax — something he had wanted to do long before the recent talks with Congress. But that is a delay not a cancellation of the tax! (He said he would try to enact permanent payroll tax cuts if he won re-election.) Also, State Aid is a huge part of what the deal was about and that is still nowhere in sight. Many economists are concerned that the economic rebound will suffer a setback following the expiration of $600-a-week jobless benefits that were a crucial component of the $2.2tn Cares Act passed at the end of March. Unemployment in the US and UK especially, is at the heart of any sustainable recovery in my view and I see a rocky recovery ahead. In the UK, While the government has been paying the wages of 9.6 million jobs at a cost of £33.8bln as of Aug. 2, it has started to wind down the program, even as many businesses are still struggling. The Bank of England last week warned unemployment will rise to about 7.5% by the end of the year. With the consumer such a large part of both US and UK economies, it is clear a recovery will be difficult with largescale unemployment and job insecurity hitting consumer confidence. As companies cut costs, those that do keep their jobs may find their pay squeezed.

It was interesting that while US stocks generally closed unchanged, the better data saw the tech sector move lower with the NASDAQ down almost 1%. It seems better data now is impacting the “stay at home” stocks. Ironically, it seems a recovery and a vaccine discovery may be bad news for FAANGS. But has the USD turned back up now? This is going to be an interesting week as that question will be discussed greatly after Fridays move in which saw some interesting formations on the charts. The EUR ended up posting a weekly “Doji” formation, a clear indication of a loss of momentum to the upside. (EUR weekly below)

The daily chart still seems to be in an uptrend but my longs may be in trouble if we break 1.1803ish. (Charts courtesy of Richard Adcock of Adcock Analysis Ltd: Thanks Rich).

I think we may find out a lot about the strength of conviction on the USD weakness this week and for now, I think the USD downtrend may return but I am not quite as convinced as I was. EUR crosses also moved lower with EURJPY failing at 125.50 resistance and EURGBP failing to close above .9050 the mid-point ma in the Bollinger bands. I will not be buying more EUR on the dip and have brought my stop up to my entry point at 1.1762 and I am exiting the USDJPY short as I may be battling against an “official hand” and have a tight stop on EURGBP as a momentum stall seems to have occurred. A lot of questions on the USD need answering this week.

To my mind the USD weakness has the Fed right at the heart of it and I see little change coming from them on monetary policy for some time and in fact, due to the sheer size of the issuance coming due, they may be back expanding that balance sheet and further debasing the USD soon. This rally may just be a gift. The question is what does this flooding of the market with printed money do to inflation in the future? The danger here is that while we are clearly in a deflationary phase and all the printed money and inflation ends up in financial markets, the danger is if and when that Tsunami of liquidity hits the real economy; then we have a problem.

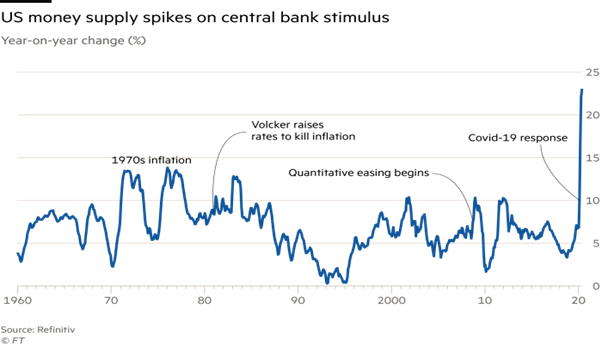

US money supply spikes on central bank stimulus

This is why the USD is lower but the impact of that is higher commodity prices at a time when times are tough. The threat of inflation is real but not yet; but those looking to hedge that risk in the future are stuck with fewer tools as the central banks dominate the bond market now. This is partly why gold and precious metals are back in vogue; “in a Pond full of negative real yields, even zero is King”! But the Fed debasing the USD looks set to continue for some time in my view and I am waiting to hear that the Fed is looking at moving from Bills to Treasuries out to 10yrs+ to soak up the supply of debt emanating from the Treasury. Right now we have a more clouded outlook between the fundamentals and the technical picture but at some point soon, maybe after further consolidation, I think the USD is probably heading down still.

The question on inflation taking hold at some point in the future is probably when and not if and that, at some point, may start impacting equity investors; at least the real asset investors and not the retail mob. I firmly believe that if we do get any sort of recovery, that the central banks and governments around the world will be slow to take back the stimulus. But that is not for now but in the future but some are starting to take some action by adding gold to portfolios. An aggressive fiscal response from the US government will be quite a boost if ever agreed and I am sure some compromise is still possible. “While we are likely to experience big imbalances in the real economy for several more quarters, if not years, the most powerful leading indicator for inflation has already shown its hand — money supply, or M2,” according to Morgan Stanley. I think a lot now depends on the fiscal boosts now as monetary policy has played its role and run its course. Doing more is pointless and I am amazed the likes of the BoE are even considering negative rates; it will not help the broad economy at all. It is fiscal spending that will make the difference but that means a massive escalation of debt which becomes the biggest threat to the system ever if rates ever start going up.

It is clear that global bond yields have remained near historical lows, even as global PMIs have moved back above 50. This matters: global investors have historically high exposure to duration. Can interest rates ever rise and if they do, will the damage to financial markets stress the system? The market value of the global bond market has risen 27% in just the past two years. Not only are there more bonds, but these bonds are longer in duration as companies take advantage of low rates and offer larger quantities of long dated debt. Over the same two-year period, the duration of the global bond market has increased by ~5%, to a record high, as both corporates and governments have taken advantage of low yields to extend maturity. With the Fed suggesting that it will shift its framework to be more dovish in the face of inflation, and recent data surprising to the upside, it’s possible that the extreme levels of real rates persist for a little while longer. But then it gets dangerous as any rises in yields is now going to impact greatly. For instance, year-to-date, consumer discretionary stocks (of which Amazon is by far the largest component) have had the highest correlation to US real rates (real yields lower, stocks up), with the technology sector close behind. What do both sectors also have in common? They’re getting larger.

At the start of 2019, these two sectors represented 24% of the global equity market. Today, it’s 30%. Globally, investors hold US$8.1 trillion more of these yield-sensitive sectors than they did just ~18 months ago. This isn’t just a US phenomenon as the EM space looks similar in construction. The damage that could come from markets even thinking rates may have to nudge higher could be rather large. But again, this is for another time but I wanted to warn you about the dangers of all this stimulus. It will have an impact and debt will matter at some point. Maybe the US and indeed the global economy can return soon to some kind of normal but that will bring the next problem clearly into view. Overheating an economy on the mend is as dangerous now as it has ever been and history shows what damage this can do. Geopolitics can also have a negative impact on assets and the US continues to prod the Tiger. The US has sent its “Health Sec”. to Taiwan under the guise of discussing Covid but I think there may be more to this. Azar is the first cabinet-level official to visit Taiwan in six years, and the highest-level US official to visit the island since 1979. The US knows how sensitive Taiwan is and the US continues to sell arms and Drones to Taiwan. This is hotting up and demands attention in my view.

In early 2019, President Xi declared during a historic speech to the Party and the Chinese people, that Taiwan would be brought back under Beijing’s sway, either by diplomacy, or violence, if need be. And any foreign powers who get int the way of that risk invoking the wrath of the Chinese people. Beijing has already protested Azar’s visit as a betrayal of America’s commitments not to have official contact with Taiwan. I do not like how this is developing and I hope it does not become a major headline anytime soon. I Trump bring us closer to physical conflict with China? I hope not.

—————————————————————————————————————-

Strategy:

Macro:.

Short USDJPY @ 105.25.. Exit trade at 105.85

Long EUR @ 1.1762 with a stop at entry (1.1762)

Long EURGBP @ .9030.. Stop at .8950ish.

Brought to you by Maurice Pomery, Strategic Alpha Limited.

—————————————————————————————————————-

Strategic Alpha Report Disclaimer

Doo Prime endeavor to ensure the reality, adequacy, reliability and accuracy of all the information provided, but do not guarantee its accuracy and reliability. All the information, analyses, comments, statements, and/or data provided in this report is for information purposes only. Client’s use of any contents of the report as the basis for the transaction, the client shall fully aware of the risks and agreed to bear all the risks. Client shall cautiously judge the accuracy of the information. Doo Prime has no liability for any loss caused by any inaccuracy or omissions of the contents and subjective reasons of Client.

Risk Warning

This information is powered by Strategic Alpha. Any opinions, news, research, analyses, prices, other information, or links to third-party sites are provided as general market commentary and do not constitute investment advice.