Good Morning… Quite a session or two recently with Gold taking the headlines last night again as it’s small exit saw something of a panic as US yields rallied and the USD turned north. But I am not sure a great deal has changed on the macro front and I have recommended a buy this morning down at $1875 (where it was when writing this). Apart from the EURGBP recommendation which is stuck, my view on the USD is mixed as I can easily see this squeeze higher extend, especially if stocks have a summer wobble which looks likely to me (which is why I have a tight stop on gold). Rising yields and a steeper yield curve could become an issue and the rise in vols across a few assets bodes ill for risk in my view. We still have a lot of issuance to come this week but the 3yr went well as yields attract. But the Fed is going nowhere and at some point I see the USD resuming its downtrend and gold should rally. Real US yields are likely to remain negative for some time and the correlation between real yields and gold is clear. But timing that is not easy and stocks may yet to have moved. Keep an eye on yields now, especially the US as they may need to be back on the risk radar. US inflation data may be worth a look later…

Keep the Faith…

Details 12/08/20

How worried should we be by the rise in US yields? Beware as vols rise. A macro look:

–

US yields are on the move and while US bonds and yields have been side-lined recently, due to the dominance of the Fed in the market, this rise should be getting our attention again. We have some serious issuance coming this week with a record $112bln being auctioned and the long end of the curve is certainly on the move with a 10bps rise yesterday in the 30yr. While selling massive amounts of debt in the middle of August would never be easy, the key here is that yields attract and attract they did in the 3yr space. The 3yr auction went well but it will be interesting to see how the auctions further out go. We saw $48BN in 3-yr Notes offered by the Treasury, a record size for the tenor with yields edging up from 11bp to 15bp in the last week to make room for the supply. The Treasury placed a record $48BN in 3Y notes at another record low yield despite the recent rebound in yields.

The market clearly believes the Fed are on hold for another 3 years; a good start to a whopping issuance week. But should we be concerned by a steeper curve and higher yields? I think we should and while the steeper curve is good for banks, the rise in yields is apparently not so good for the tech sector which again lagged others. It is not good for gold, commodities or those short the USD either and gold got hammered yesterday and the rout continued overnight with a low at $1864 seen.

This has seriously changed the outlook on the technical picture with the MACD crossing back down and the mid-point of the Bollinger bands broken and closed below. Volatility in many assets is on the rise and equity investors should be wary.

This rise in yields, especially in the long end, caught the attention of precious metals and gold fell $100 through $1900 and kept going; a signal to us all? I have mentioned how small the exit door can be in gold before but I am quite surprised US stocks did not react to this more than they did but the NASDAQ under-performed again; but they may yet as higher yields and a stronger USD are not great news for stocks either. It is not yet known if this is a blip in gold and some of the specs are getting squeezed but if the Fed is on hold for 3 more years at least, then US real yields are staying down and so after a clear-out, gold may recover but it could be an early canary warning of risks ahead in my view. The link between real yields (inverted below) and gold is clear.

This issuance is huge and if a further deal is struck between Democrats and Republicans, more debt will be pushed onto the market. Of course, this raises a question on how they ever get past this debt and in reality, they will face 3 options; 1) they can default on their debt (not really an option); 2) Inflate it away or 3) impose sufficient austerity to slowly pay it down (also probably not an option for a government that wants to stay in power). So that leaves option 2.

Number 2 is another reason why gold may find some friends again somewhere down here and I am prepared to dip a toe in here and buy at current levels ($1875.00) with a tight stop below $1820). This also feeds back into the USD and with a deflationary outlook in the short-term and real yields set to stay negative for some time, this USD bounce may well turn out to be a gift but we may have to wait, as again the market is short and vols may pick up. But what impact would a surprise rise in yields do to the USD? The future, with inflation as a problem, seems a long way away right now but things are shifting. The danger here, or the irony if you like, is that it is the reflation story that could send bonds tumbling and yields racing higher; what will that do to stocks? Not good news I would think and there was another early reflationary canary as the last two days has seen a surge in beaten down value stocks at the expense of bond-like tech/growth stocks. I think USTs are about to become important to have on your radar again.

US10s now yields .0655% (chart above a few hours old). At present, this rise is modest and has not really caught the attention of markets apart from gold and some other commodities but I would keep an eye on this.

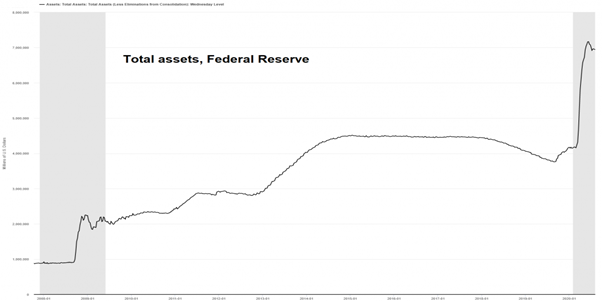

If you ever wander onto the Fed website, you may come across an explanation of the Fed’s balance sheet. It states that “The Federal Reserve’s balance sheet has expanded and contracted over time. Really? Not for a very long time it hasn’t.

And the danger is it is about to expand further if they have to step in to hoover up what’s not taken in the long-dated auctions this week or next quarter. Again, I think the Fed policies are at the centre of so much that is wrong right now and is why faith is being lost in the USD. Yes, $700 billion was contracted from the Fed’s Balance sheet between October 2017 and August 2019. But that was in the wake of a $3.5 trillion expansion and it was quickly followed by another $3 trillion balance sheet expansion this spring. There is likely more coming and why would anyone save? The worth of the USD is eroding and may continue for a while. This rally in yields, may not last past this week if the Fed decides they need to keep a lid on yields and looking at the issuance, they may be forced further down the curve into USTs again. The point is that the Fed seems to have made up its own new mandates that include keeping the Treasury and the big banks flush with cash and making sure stocks don’t get mangled as it would cause a deeper recession, or worse, as they forced everyone into these risky assets. They are complicit in making the USD worthless by flooding the markets with printed dollars. Is the move into precious metals and commodities a rush out of Dollars?

Stocks also need to realise that Trump has only put a plaster on the bail-out issue and that Congress still cannot seem to find an agreement on how to help the millions relying on the benefits that run out last month. This has huge implications and almost no one thought they could not find a compromise. There is a little time left but not much before panic starts to set in. The two parties have not even spoken on the subject together since Friday; what are they waiting for? On top of this, a vaccine is still some way off (despite what Putin thinks) and cases are re-emerging even in places like NZ who sounded the all-clear! Unlocking without a vaccine still has its risk and NZ is locking down Auckland again. Stocks in Asia were lower and led convincingly by Shanghai which fell over 2% last night (pressured by data showing domestic bank loans fell more than analysts forecast in July) and NZ down 1.3% with marginal losses in Oz, HSI and Kospi (the Nikkei marginally higher on a weaker JPY).

Right now, the NASDAQ is still in an uptrend due to late buying in the last few sessions but it could be showing early signs of rolling over. August is a tough month with a lack of liquidity and with US stocks up close to record highs, taking some off the table makes sense with all the concerning signals and rising vols in other assets. If we do see a wobble in global equities, the USD squeeze higher may continue for a bit and I will watch price action closely here.

The other thing that equity investors seem to be ignoring is the breakdown in relations between the US and China. The US continues to cross “Red lines” over Taiwan as far as China is concerned and US health secretary Alex Azar has raised the possibility of a trade deal with Taiwan during a historic visit to the country this week in remarks that are likely to trigger protests from Beijing. On Monday, as Azar headed into a meeting with President Tsai, Chinese fighter jets crossed the Taiwan Strait median line, an unofficial dividing line between the two countries. Both sides have traditionally respected the line to avoid conflict. But the Chinese military has begun violating it regularly this year. Phase2 of the trade war is in full swing and I can see this testing the resolve of both parties and I just fear how far Trump is prepared to go to look tough on China in order to gain support at home in front of the election?

The macro look. This is not a usual recession as things like income growth have risen and not fallen due to massive fiscal injections directly to the consumer. At the same time the Fed has slashed rates and has ballooned its balance sheet, which we now know hinders growth. In fact, the outcome of the recession will ultimately be worse as the level of public and private indebtedness has breached all critical thresholds and will now have a non-linear impact on economic growth and we may be facing the weakest expansionary income growth in the years to come. Prior to the COVID recession, the average recession brought income growth of -0.54%. In other words, incomes declined during the average recession. In 2020, due to one-time stimulus checks and massively boosted unemployment benefits, so far, we have seen 32% annualized growth in income during the recession but these are a one off payment.

To put this in perspective, total government transfer payments reached a record 30% of total income during the crisis and has since cooled to about a quarter of total personal income.

I am not sure at all, that embracing MMT comes without significant side-effects. Many have pointed out that this is akin to a “free lunch” as long as the Fed buys the debt issued to the public. This is a highly flawed analysis that disregards many core pillars of macroeconomics and a careful study of the existing problems associated with extreme levels of over indebtedness. Is there such a thing as a “free lunch” in economics? I think the payment will have to be made at some point. Government debt as a % of GDP has risen to levels that are significantly above the threshold for diminishing marginal returns yet we continue to believe that more is more, dismissing the evidence that more government debt, regardless of the use and the balance sheet on which it resides, will have a nonlinear negative impact on economic growth. We have seen this played out in Japan and to some extent the EU where QE and monetary policies, once rates get close to zero do nothing to increase growth.

Debt is simply a pull-forward of future consumption or rather an exchange of current consumption at the expense of future consumption (stealing from our children). We are in the process of the greatest pull-forward of demand in history and we continue to believe that because we are using “more” debt, or that because it is directed to a particular group of people rather than another group, that we can bypass the well-documented evidence of diminishing marginal returns. No, there is no “free lunch”; you will just be getting the bill later in the post. The danger here is that governments try and extend the “one-off” benefits as rising unemployment and the lack of spending on non-essentials remains a threat and debt increases even more but this cannot go on. Now that we have pulled forward income growth into the recessionary period to plug a record output gap, the economy will struggle to gain its footing independent of government support. Maybe the outlook from the 3yr auction is right and that Fed rates are on hold for 3 years. But the velocity of money will not be seen unless governments keep handing out gifts directly to the consumer and that cannot go on for another 3years surely. At some point, all this will matter but policies are not impacting as they used to and yet they keep doing more. One day we will run into our future and our children will ask why!

—————————————————————————————————————-

Strategy:

Macro:.

Long EURGBP @ .9030.. Stop at .8950ish.

Long Gold @ $1875 Stop at $1820

Brought to you by Maurice Pomery, Strategic Alpha Limited.

—————————————————————————————————————-

Strategic Alpha Report Disclaimer

Doo Prime endeavor to ensure the reality, adequacy, reliability and accuracy of all the information provided, but do not guarantee its accuracy and reliability. All the information, analyses, comments, statements, and/or data provided in this report is for information purposes only. Client’s use of any contents of the report as the basis for the transaction, the client shall fully aware of the risks and agreed to bear all the risks. Client shall cautiously judge the accuracy of the information. Doo Prime has no liability for any loss caused by any inaccuracy or omissions of the contents and subjective reasons of Client.

Risk Warning

This information is powered by Strategic Alpha. Any opinions, news, research, analyses, prices, other information, or links to third-party sites are provided as general market commentary and do not constitute investment advice.