Good Morning.. A rather brutal end to the Asian session overnight, as it appears that over the weekend, virus infections are on the rise in US states, China and India. Chinese data helped little and markets turned sharply lower with S&P futures breaking below 2950 which many felt would be a range base. As I type, EU cash equities are just opening but I do note that bonds, whilst higher, are not showing the same stress as we see in equities and USDJPY has hardly moved. It will be interesting where we go from here but we may have a busy week ahead with the Johnson/EC video call today, Powell testifying tomorrow and the BoE Thursday. Trade accordingly. Position recommendation remain the same but the EUR position looks at risk with the stronger USD and in case we do get a compromise of sorts from Brexit talks, I have raised the stop in EURGBP up to .8900.

Keep the Faith..

Details 15/06/20

US equities close higher Friday; why did it feel like a down day? Brexit video call.

–

The S&P managed to eek out a 1.3% rise on Friday but the session seemed to me to feel like a negative day; an attempt on 3000 in the S&P failed again but I think that support has now gone after fears of a second wave of infections in Chin and parts of the US, saw equities in Asia slump again and I think US equity markets may be in for a shock.

US yields were higher Friday and I think that was partly why US equities held up but we have seen US yields fall overnight with USs 10s down 4bps to 0.66%. All rather confusing and a typical Friday to be honest but clarity is appearing this morning as we see clear risk aversion building. The market is starting to focus back on the Virus stats and to be honest, from China to the US and India, they are far from encouraging as reinfection is taking hold after unlocking of economies.

I think one thing is also becoming clear and that is that investors are starting to realise that all the furloughing of staff does not guarantee a job to go back to. Businesses will be forced to cut costs and that means jobs and again I bring this back to the forefront of the conversation: The consumer matters. I still think there is a gulf between reality and where stocks are priced and there is a real danger here of a significant move lower now in global equity markets. The retail bid has finally been tested and my view is that any further weakness now will see a new wave of capitulation. I remain rather risk averse and see further gains for EURAUD, possibly EURGBP but EUR, with the rising USD on risk aversion, looks threatened. USDJPY looks way too high but grasping what drives that now is something rather complex.

EURAUD daily above and a close above 1.6500 should spark a move towards 16860.

Meanwhile, Europe is reopening and there is some hope that this will save many tourist-based economies; but will the tourists be prepared to travel, are restaurants really going to get back to where they were, or hotels, or airlines? Unlikely, as many are going to wait and see how things pan out. Will all the furloughed employees all get their jobs back; I hear in the UK of small businesses forcing pay cuts on senior staff. Companies have lost so much revenue that cost cutting is inevitable. In the markets, the VIX sitting at 42 tells a story and I think markets are about to start pricing some reality for the first time in a while. To my mind the euphoric, retail-based rally is in some trouble.

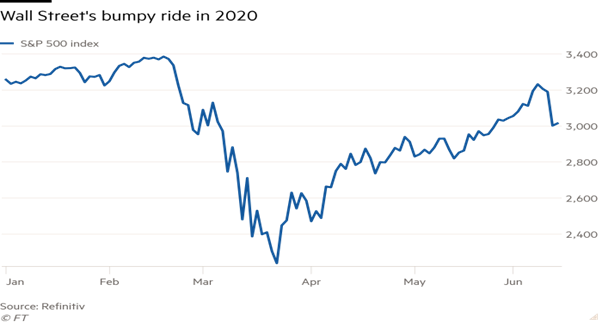

Line chart of showing Wall Street’s bumpy ride in 2020

What many thought was a one-way bet, just became a two-way bet and the s/t spec market is long up to their teeth and probably leveraged too. It is time for a reality check; and US earnings are on the horizon. So far, we have seen a serious rotation in stocks rather than any wholesale dump as many investors in the asset management community have to stay invested in stocks as the alternatives are minimal; cash almost not an option with yields here. The real crash will come if the rotation stops and we see a wholesale capitulation but so far, that is holding.

While I get the fact that the Fed and many central banks have gone all-in on providing liquidity for the markets and some rely on the Fed to support markets at all costs, that does not mean that equity markets cannot have “one of those days” as seen last week with a 6% fall on Wall St and in my experience, these moves rarely happen in isolation. Yes, the Fed and the US government has done a huge amount to save the economy but do we need to question this? Who is it helping and where is the benefit to the man on the street in coming months? A lot of the government bail-out schemes are due to end in late July; then what? The main central banks’ balance sheets (the Federal Reserve, Bank of Japan, European Central Bank, Bank of England and People’s Bank Of China) have soared to a combined $20 trillion, while the fiscal easing announcements in the major economies exceed 7% of the world’s GDP, according to Fitch Ratings. This is the biggest combined stimulus plan in history and no matter what the central banks say, they are now clearly monetising debt as the chart of the US below clearly shows.

There’s been a fundamental change in how governments tax and spend, yet most do not yet realise it; MMT is going mainstream with unknown consequences. However, businesses are closing at a record pace and unemployment has reached extremely elevated levels in many countries. This begs the question; can monetary policy and government spending actually fill the gap? I am not sure it can if unemployment remains higher and longer lasting than expected. When one looks at the extreme monetary policy of Europe and other countries with negative rates, all I can ask is how can anyone claim with a straight face that monetarism is working for us. So, I guess CBs feel they would rather try something new than continue down the current road of easier and easier monetary policy.

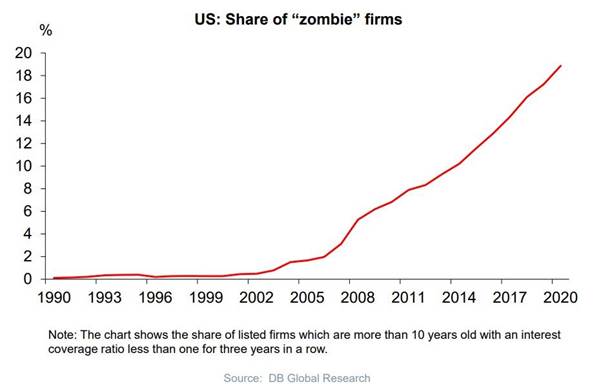

So, what are these policies producing? The problem I have is that while viable businesses are falling by the wayside, it is the Zombie companies that seem to be kept alive. This is nuts! According to the Institute of International Finance (IIF), the figure of global corporate bond defaults has risen to $50 billion in the second quarter of 2020 despite historic-low interest rates and high liquidity. Additionally, according to Deutsche Bank and the BIS, the number of zombie companies in the eurozone and the US, large companies that cannot cover their interest expense costs with operating profits, has rocketed to new all-time highs.

Yet again it seems that the CB printed money is going to the wrong place. I will not dwell on this for long as it is a tad macro but the rise in bond defaults is a consequence of previous high leverage in a weakening operating income environment. This should not be a concern if creative destruction works to improve the economy, as inefficient companies are taken over by efficient ones and new investors re-structure challenged businesses to make them competitive. That is called capitalism. The big problem is that massive liquidity and low rates are perpetuating overcapacity and keeping an extraordinary amount of zombie firms alive. What are the central banks creating here?

I fear that we have entered a phase where the markets no longer function as they should due to interventions by central banks which are meant to stabilise these markets and revert them to a normal baseline but in fact create some serious side effects which the CBs may not be able to control. I still think we are ignoring the fact that what happened in 2008 is still with us; it has just been moved down the calendar and disguised by central bank activity. When the reality of that dawns, then things change rapidly. The danger here is that while central banks and governments have gone all in, job losses continue and the modern economies slump still. But the issue is that the central banks are stealing our free markets and replacing them with a socialised structure. They control massive segments of the “free markets” now; will they ever give them back? I think two of the biggest questions out there now are 1); how long will the recovery and unemployment take to recover and 2) just how temporary are these central bank policies?

We, as market professionals, have a lot of faith in our central banks and from an early age we are told “do not fight the Fed”. But can we be sure that in these unprecedented times and untested monetary policy actions, they are doing the right thing? Again I come back to the abject failure of the BoJ to hit any of its goals through monetary policy over almost 20 years and the same can be levelled at the government too with fiscal policy. Right now, in the US at least, markets have taken the side of the Fed but are we about to find out that after all they have done; it is NOT enough? What if, after all they have thrown at this, the economy fails to reignite and markets fail? Or what if we do get a recovery and the central banks and governments withdraw the drugs? This is by far, not the first crisis we have faced recently and as I have said, I see this as part of the on-going 2008 problem but with every new crisis, problems have become deeper and more difficult to manage, which was to be expected in a world in which constant bailouts from central banks prevent a normal corrective process to occur as the imbalances and excesses continue to pile up resulting in ever greater shocks to the system, requiring ever greater bailouts and even greater debt. We have NOT fixed the underlying problem! We do not have a cure for the virus or the economic imbalances from 2008 which remain in place.

This begs an interesting question, as to my mind, the central banks are going to find it hard to take back any stimulative policies without causing a market crisis. The irony is, on a macro basis, that this causes the next crisis! But what if it creates the inflation part without the growth part? Stagflation is an ugly word seldom used in central bank circles as it is a structure that monetary policy cannot deal with. It seems to me that the very cure the central banks crave (rising inflation), may end up being a disaster of a different kind. With markets holding central banks hostage now, the danger is the bubble expands and Icarus flies ever closer to the sun. Where is the escape route for central banks? If we get through this crisis and policies remain in place, the next one will be fought from an even weaker starting point. Markets price no normalisation at all from the Fed but what happens now if global equity markets, for whatever reason, start falling precipitously? Many feel that is impossible but I have been in these markets long enough to suggest nothing is impossible. Maybe we are in a trading range now for the S&P between 2950-3250 but I would be very careful if we break any lower.

I have to say this again, as it seems to be getting lost; Equity markets are NOT the economy. Quite simply, there is a ‘Great Divide’ happening between the near depressionary economy versus a surging bull market in stocks. Given the relationship between the two, they both can’t be right and one is likely to break. Again, over the many years I have been in these financial markets (and I have yet another birthday looming tomorrow), I have witnessed that the reality is, that the economy is the real decider in all this over time. (There is a close relationship between the economy, earnings, and asset prices over time.). Yes, we get extensions based on euphoric markets but the reality usually dawns at some point but as ever in this business; timing is everything. But I think we may have had a tremor and the real shock may still be to happen. Was last week a warning and is the volcano smoking? Global stocks have a sentiment and psychological aspect, which allows divergence from reality but the underlying fundamentals do resurface in free markets. The question now, is whether the US still has free and functioning markets I guess. If it does, then look out.

Meanwhile PM Johnson takes up the Brexit fight in earnest today, as he holds talks with the European Union’s top officials, with both sides looking to reset negotiations that have drifted into stalemate. I think some tough talking is on the cards and maybe there is room for compromise but I find it hard to see where. If talks do not go well today, then I think there is a danger that the markets start pricing in a greater chance of a hard exit and I remain of the view that Boris is prepared to walk. Having said that, both sides need a deal and in the event of some compromises, I think GBP will rally quite hard and so I am bringing the stops up in EURGBP to .8900; just in case. No breakthrough is expected from the video call between Johnson and the presidents of the European Commission, Council and Parliament. The meeting is a requirement of the Brexit Withdrawal Agreement and will be a review of its implementation and the progress of the trade talks. While both sides speak of it as an opportunity to inject fresh impetus into the proceedings, officials say Monday’s conversation won’t be a forum for negotiation. But we may get some interesting rhetoric afterwards.

I think many feel we are seeing tough negotiation skills being used to get a deal and that a breakthrough can be found which is the way the EU works; try and delay but compromise at the 11th hour. I read in the press that while politicians and officials have struck a pessimistic tone in public, privately they are more positive. If discussions can make progress in July and August and wrap up in September, EU leaders could be asked to ratify a deal at their scheduled summit in October. That is a big IF as both sides are still far apart, with each accusing the other of refusing to engage on fundamental issues and both sides seem to have some no-go areas where they refuse to budge. The U.K. still rejects the EU’s demands for a level playing field, which would bind Britain to some European rules in areas such as state aid and environmental law. It is reported over the weekend that PM Johnson will tell EU leaders he wants a deal by autumn at the latest so that firms can be given certainty about the UK’s exit from the EU. But it remains clear that the two sides are also at odds over law enforcement cooperation and how any agreement should be structured. It will be interesting to see how combative both sides emerge from todays video call.

Following the UK’s formal announcement on Friday that it would not seek to extend its post-Brexit transition period beyond the end of this year, both sides will stress the urgency of ending the stalemate in the future-relationship negotiations, which have made little headway after four rounds. They simply have to get on with this now. If EURGBP breaks the recent highs close to .9045, then we may see a further leg higher.

—————————————————————————————————————-

Strategy:

Macro:.

Long EURGBP @.8978 added @ .8940. Stop at .9000

Long EUR @ 1.1360.. Stop at 1.1200ish. Added at 1.1285.

Long EURAUD @ 1.6260 added at 1.6500. Stop now at 1.6260.

Brought to you by Maurice Pomery, Strategic Alpha Limited.

—————————————————————————————————————-

Strategic Alpha Report Disclaimer

Doo Prime endeavor to ensure the reality, adequacy, reliability and accuracy of all the information provided, but do not guarantee its accuracy and reliability. All the information, analyses, comments, statements, and/or data provided in this report is for information purposes only. Client’s use of any contents of the report as the basis for the transaction, the client shall fully aware of the risks and agreed to bear all the risks. Client shall cautiously judge the accuracy of the information. Doo Prime has no liability for any loss caused by any inaccuracy or omissions of the contents and subjective reasons of Client.

Risk Warning

This information is powered by Strategic Alpha. Any opinions, news, research, analyses, prices, other information, or links to third-party sites are provided as general market commentary and do not constitute investment advice.