Good Morning. Markets are likely to be quiet this afternoon with the US out on holiday but we had a rather mixed session in Asia with China stocks rising on policy easing while Nikkei fell on the back of much weaker GDP data. GDP is rather backward looking but this bodes ill for PMIs later this month as the virus impact is still with us. PMIs from the EU and UK will make interesting reading on Friday. Data from the US was mixed Friday but Trump is talking more tax cuts to buy votes. US markets are still attracting capital and so this USD may rise further in my view and may even get a little less predictable soon. DXY above 100.15 may see a race higher. The global industrial recession is deepening and demand is waning. Deflationary instruments from oil to commodities are falling steeply and bonds are bid globally. CapEx continues to fall in the US while equities push ever higher; something is going to have to give but when? Are investors becoming irrationally bullish now? I note with some interest that the start of this year has seen less equity buyback volumes (see below) and they have been a massive prop for US markets in particular. Should be a quiet one barring headlines today but across Asia we see growth forecasts being cut.

Keep the Faith..

No data of note today.

Details 17/02/20

Mixed data so Trump prepares to buy votes: US holiday:

US data has suggested that the US is still way ahead of the rest of the world and they have a central bank that seems poised to act if any signs of a slowdown are seen. The data Friday was mixed as the hope and expectations of the consumer saw gains, while the reality of retail sales seemed to suggest something else as the Control Group came in disappointingly flat from the previous month and we saw revisions lower also. But February UMich Sentiment rose for the 6th straight month to its highest since March 2018. To say the data was mixed on Friday would be something of an understatement and there was something for bulls and bears. It is also clear that the global manufacturing recession is hitting the US as well but the US economy is not so reliant on this as many others are.

US Industrial Production has contracted year-over-year for 5 straight months and Capacity utilization was also rather concerning.

If Caterpillar is still the global industrial bellwether and leading manufacturing sector indicator it has been for the past century, then the world is about to enter the worst manufacturing downturn since the financial crisis.

According to CAT’s latest retail sales data, in January the company posted a 7% drop in machine sales, the biggest drop since Jan 2017, and only the second consecutive negative print since December’s -5% drop following 33 consecutive months of increases. But markets do not see this manufacturing recession as relevant! Exporters are really starting to feel the pinch, especially in Asia and Germany. In Japan, gross domestic product shrank at an annualized pace of 6.3% from the previous quarter in the three months through December, the biggest slide since a previous tax increase in 2014, according to a preliminary estimate by the Cabinet Office released overnight. Economists surveyed had predicted a fall of 3.8%, flagging the adverse impact of the tax hike, weak global demand and typhoon disruption. Things are getting nervous in China and the PBOC continues to add liquidity as last night it said it was lowering the rate on 200billion yuan ($28.65 billion) worth of one-year medium-term lending facility (MLF) loans to financial institutions by 10 basis points (bps) to 3.15% from 3.25% previously. No MLF loans had been set to mature on Monday.

We may start to see the impact on survey data from the virus threat and this could be important, especially for the likes of Germany and indeed the rest of the EU. On Friday, IHS Markit will release composite purchasing managers for the eurozone and its two biggest economies, France and Germany. These will provide a snapshot as to how the region’s companies are faring and could offer an early clue as to how severe the impact will be. January’s reading for the eurozone hit a five-month high, suggesting an upturn in the bloc’s fortunes but February’s survey will give a much better picture of any fallout from China’s shutdown and fears over the virus. The forward-looking survey data from around the globe will be monitored closely. Is growth in the EU grinding to a halt? UK PMI data is also expected and it will be interesting to see if the post-election sentiment rise is still there. Confidence seems to be holding in the housing sector at least.

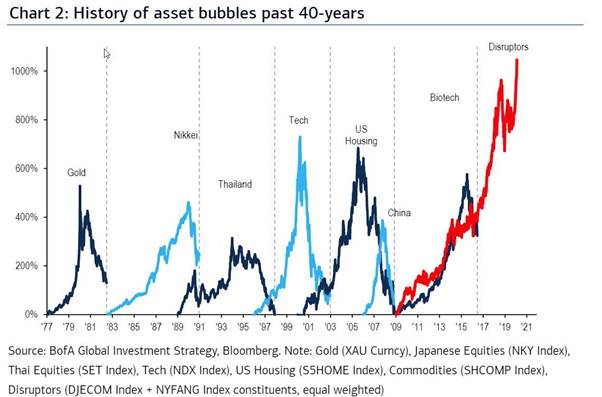

All this as central banks have cut interest rates 800 times since the 2008 crisis. Not much return for that considering the QE or printed money also shoved into the system. Where is the growth? What has been achieved is asset inflation and nothing else according to BoA. The “deflation” assets, such as bonds, credit, growth stocks (315%), have massively outperformed inflation assets, e.g., commodities, cash, banks, value stocks (249%) since QE1. At the same time, US equities (269%) have massively outperformed non-US equities (106%) since launch of QE1″. They are quite right; the central banks have completely missed their goals. No wonder we have seen such strong stock markets as central banks have destroyed yields even in high risk instruments and they should be held to account when, not if, this implodes.

Is this the biggest bubble ever?

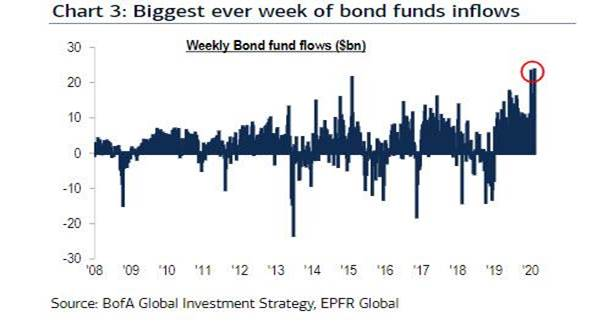

The issue here is that it may continue as Trump is now talking of tax cuts to help Americans buy more stocks! Again, as in so many parts of the developed world, larger debt mountains are for anther time in the future when current politicians are long gone; they simply are stealing from our children, as indeed we are regarding the planet. The morals behind this stink. The issue with Trump extending the economic cycle with more spending is likely to keep attracting foreign capital and I can see this USD rising further and a break above 100.15 and possibly 101.00 in the DXY looks likely to me, especially if this EUR weakness continues. But at the same time, we are seeing massive bond inflows as well which is a little confusing and commodities are getting hammered. One would expect to see bonds, oil and commodities getting hit on economic slowdown and potentially a deflationary scare. Just last week investors poured the most money ever into IG corporate bonds ($13.4BN). Cash is clearly NOT an option for asset managers.

Are investors becoming irrationally bullish now? That is when things can get ugly but standing in front of this is painfully expensive.

At this rate, bond yields could hit the lows again and this has been the surprise to me while stocks continue to rise. Where is the low in US yields? I think we need to be aware that a top in risk assets could be seen and possibly if this USD does really start to move higher at pace but it appears Risk Parity funds are growing and they buy equities and bonds; maybe that is driving this anomaly. Any potential peak in equities may not be until Q2 but I am watching markets very closely now for some disorderly moves; vols look a little low to me in some instruments; FX especially so. US stocks have been dragging in capital but have also massively benefitted from gigantic share buyback schemes. Stocks will struggle to sell off far while that is the case but there are some data starting to emerge that suggests buybacks may be starting to slow. The data suggests that announced buybacks were off to a much slower start then we’ve seen in the last 5yrs. Jan came in below $10B, vs. an avg. of ~$50B the prior 4yrs.

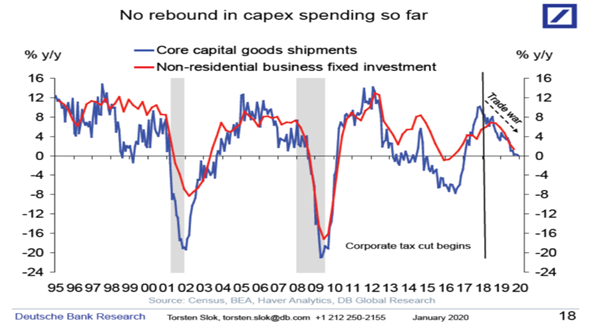

If we ever get a hint of peak buybacks, then look out! Maybe bonds, commodities and gold are telling us that investors do have concerns; they just do not want to give up on stocks yet. The US stock market is the world’s “darling stock market” and capital is still flooding in; TINA. But CapEx matters and the consumer is spending borrowed money.

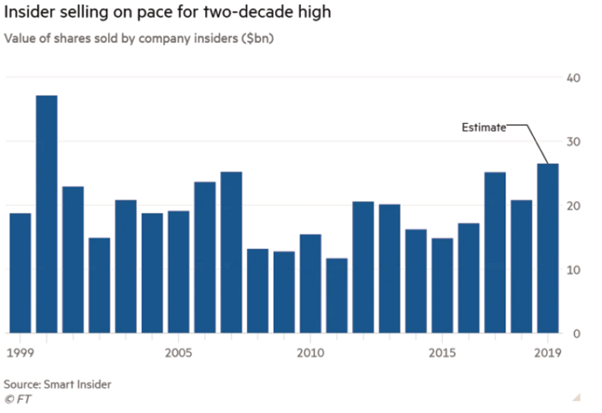

Not everything in the US economy is rosy and at some point, investors will be tested and so too the central banks who, by the way, have little ammunition left; no matter what they tell you. Given how unreliable leading equities benchmarks are as a gauge of global economic health, riskier and more macro sensitive assets, such as commodities and emerging-market currencies will probably offer a more useful guide and there we see what could almost be called distress. Buybacks are no guarantee for investors though, as GE has clearly shown and since 2013 Boeing has splurged on $43 billion in repurchases: now look at it. It’s all about shareholders now and not the businesses future; now Boeing appears to be on the verge of compounding its previous errors by borrowing money to pay dividends at the same time that it is reducing R&D spending. Equity buybacks up here are a huge risk in fact. Oh, and while all this is going on, insider selling (those CEO’s and corporate CFO’s) are selling at almost record levels!

Makes you wonder why really; doesn’t it?

—————————————————————————————————————-

Strategy:

Macro:.

Short AUD @ .6875 at .6917 (average .6896).

Short USDJPY @ 109.95.. stop above 110.35 (s/t position just in case).

Short EURJPY @ 119.45. Tight stop above 120.20.

Macro Long FTSE250 20,900

Brought to you by Maurice Pomery, Strategic Alpha Limited.

—————————————————————————————————————-

Strategic Alpha Report Disclaimer

Doo Prime endeavor to ensure the reality, adequacy, reliability and accuracy of all the information provided, but do not guarantee its accuracy and reliability. All the information, analyses, comments, statements, and/or data provided in this report is for information purposes only. Client’s use of any contents of the report as the basis for the transaction, the client shall fully aware of the risks and agreed to bear all the risks. Client shall cautiously judge the accuracy of the information. Doo Prime has no liability for any loss caused by any inaccuracy or omissions of the contents and subjective reasons of Client.