Good Morning.. A quiet Asia session with tight FX ranges but FX has been interesting over the last 24hours. Yesterday it seemed the inverse correlation of the USD to risk assets broke down. I am not sure if this will last and to be honest the USD is lower as stocks have rallied but it caught my eye (see below). We didn’t get much from Powell that we didn’t already know and I doubt he will add anything today when in front of the House. It does seem that the market is grasping the fact that central banks, led by the Fed, will allow asset bubbles if it is a side-effect of bridging this crisis. CBs are monetising debt quite openly now and I think this will see the BoE add to their QE programme tomorrow. I am going for £150bln as why do less and have to top it up again in August? Geopolitical tensions kept AUD down yesterday but to be honest I think a few sold the USD as stocks rallied only to hit a wall. The USD direction is less clear here. EU CPI this morning and Canadian CPI this afternoon are the highlights in the data but data. To date, data has been ignored but it seems we had a reaction to US Retail Sales data yesterday; is the US recovering faster than the RoW and does that mean US assets and the USD attracts again? It is early days yet to make that assumption but it was an interesting day yesterday. Could be a quiet one today..

Keep the Faith..

Details 17/06/20

A few things caught my attention yesterday. What happened to the inverse USD correlation with risk? BoE meeting:

–

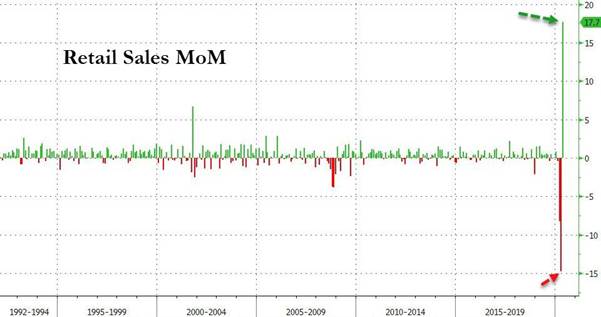

It was a fascinating trading session yesterday with a bit of everything in it; we had positive US data in the form of retail sales, the Powell testimony, a strong rally in global markets and a sell-off in the middle of the US session on renewed Covid concerns in the US. The equity market rally was a strong one for most of the day after a strong performance in Asia but interestingly, the BoA Fund Management Survey, showed that 78% of funds saw US equities as overvalued. That is intriguing and while they may be right, it may also suggest that they are not long or even short! Also, according to the BoA FMS, while 37% now say “it’s a bull market”, 53% majority still say, “it’s a bear market rally”. While we digested this, yet again we had some bad news as virus cases leapt in parts of the US and we found ourselves battling yet again between Fed stimulus on the one hand and virus second wave concerns on the other. That is on-going. But again, after the equity fall from the highs, it seems there remains a demand to buy the dip. In addition to all this it was announced in the UK that a globally available and cheap steroid drug may reduce deaths from the virus by up to 30% and is a huge news if the case and studies look very convincing. What a day but to be honest I have been saying that for the past week or so.

We also have some geopolitical events brewing as an explosion on the Korean border looks like an attack on a building by N. Korea in the DMZ and stories emerged of casualties from an on-going skirmish on the Indian/Chinese border. As many as 20 dead according to the Indian version of events but an event that seems to have escaped the notice of the Chinese. But markets still seem motivated more by what central banks do and in particular the Fed but to be honest, Powell stuck mainly to the FOMC script. But the active involvement in corporate bonds did not go unnoticed as spreads collapsed and HYG and LQD had significant moves. As I said yesterday, these markets were NOT stressing and so the timing was questionable unless you look at where stocks were when they announced it. I am not saying we should all jump in a buy equities, as there clearly are risks out there but what I am saying is the dips should hold as there is a clear commitment from the Fed to hold markets up.

The other thing that struck me through the session was the detachment of the USD to a risk on move. Yes US yields rallied steeply and the curve was steeper but we have seen that before recently while the USD fell on a risk on move. It was blatantly clear that as stocks rallied after the strong and impressive US retail sales data, that the USD was bid and remained that way for most of the session and indeed overnight.

Make of it what you wish from this mad chart. I was scrambling around looking for why the usual inverse correlation with risk was no longer there. I wonder if this was due to the fact that global investors feel the US may be the first economy accelerating out of the recession and therefore attracting capital back into US assets and thus a demand for USD’s. I m not sure if this will continue but it seemed to fit what was happening over the last 24 hours.

I would think a lot of investors bought the likes of EUR or AUD on rising equities only to find a wall of selling and all of it after the US data release. Having said that, as stocks have risen this morning the DXY made new session lows; all very confusing. Meanwhile, I guess many will now be asking how far Powell will allow stocks to keep rallying before screaming the risks out there. But the issue now is that the Fed seems to believe a wholesale sell-off in US equity markets will create an economic storm that they want to avoid and that is the key here. Like it or not, that now seems to be a fact and if we look back at everything Trump has demanded of Powell, with zero rates and massive stimulus programmes, he has delivered to his master.

All this monetary stimulus from the Fed is all very well and probably much needed in this crisis but what is missing (and is a huge concern of mine), is a clear exit strategy to mitigate a risk of uncontrolled deficit spending with commensurate monetary expansion and, ultimately, inflation at some point in the future. There is no talk anywhere at central banks of how we get out of this as we all know how reliant asset markets are on central bank support. It is front, middle and back of why stocks are up here. The lengths and depths of their interventions indirectly into equity markets by directly buying high yield and now corporate bonds is a perversion of the financial system. No red line shall remain uncrossed it seems. That is a green light to equity investors and Powell knows it.

I think that with an elevated VIX and on-going virus headlines, we may see quite a few wild swings in equities but as I said yesterday, I think the central banks are now determined at all cost to hold them up until we get through this crisis. That is a game changer for me and coupled with the government stimulus still to come, they may pull it off in the short-term. But can they ever reverse all this? The issue is when it matters, not if. Debt has been a growing issue since Nixon took us out of the gold standard, so if governments can get away with it, I think they will soon be insisting the printing presses hum along. They are buying themselves longevity in office and will buy their way to bridging this crisis. Social welfare schemes will get massive boosts into elections to buy votes and this is how populist politics works. Mention austerity and you are politically dead. There are no bond vigilantes now and the economic and political landscape has changed. That means that investing processes need to be re-examined as analysis based on the past may find you underperforming. Powell is likely to keep his foot on the gas until he gets unemployment back below 5% ish but that could take a very long time. As Powell said last week, liquidity will continue to be injected as long as it “preserves” jobs even if it means pushing risk assets to nosebleed bubble levels; get used to it. The Fed and central banks around the world are prepared to absorb any shocks to the system, even if it means inflating asset bubbles.

If it wasn’t for the Fed activity in USTs, things would be very different. Foreign investors (including central banks, governments, companies, funds, and individuals) shed $44 billion of US Treasury securities in April, compared to March, according to the Treasury Department Monday afternoon. Over the same period, the mountain of US Treasury securities grew by $1.287 trillion. Someone must have bought this $1.287 trillion in additional US debt that was issued in April, plus the $44 billion that foreign holders dumped. This amounts to $1.33 trillion. But who bought it? It has to be said that buying Treasury securities is a far more unpalatable undertaking today than it was when rates were at 2%. The yield ranges from near-zero for short-term Treasury bills to 0.7% for a security with a maturity of 10 years, and up to a “whopping” 1.45% for 30 years. Inflation will reduce the purchasing power of the principal by more than the interest paid. And yet, there is demand for them, or else the yields would spike as prices plunge. But who are the entities buying them? No prizes for guessing. Over the two-month period of March and April, the US government increased its debt by $1.56 trillion (most of it in April); and over the same two-month period, the Fed bought $1.56 trillion in Treasury securities (most of it in March) and thereby monetized 100% of the additional pile of debt during the two-month period. And they tell us they are not monetising all the debt; pah!

Tomorrow we get the BoE meeting and it looks pretty clear that the new Chair is as open to more stimulus as the last and it looks likely we shall see an extra £150bln boost to the QE programme that will do absolutely no good to the broad economy at all with rates already at zero (some suggesting £100bln but why not go large?). This is about preparing the BoE to be able to monetise the debt on its way down the pipe as the government tries to spend its way out of this crisis. With bond purchases at their current rate, the QE programme is set to run out in early July, so it is pretty clear that an extension will be on the cards with the only uncertainty over the amount. (Why add £100bln only to have to top up again in August?) With the BoE ready to take up the slack in any Gilt auction, the government, based on MMT, can keep spending. On the question of negative rates, the UK is in a position to monitor what impact they have had on other economies but while they may endorse this at some point, it would be seen as something of a shock at tomorrow’s meeting as a review is on-going and markets are not pricing them until June2021. Will the BoE look hard at corporate bonds and look to add help there too? Let’s face it, waiting may not be a great option if they feel these policies could help now.

On monetising debt it is no longer credible that central banks like the BoE are suggesting this is not taking place as we are not stupid. Since the March 19 meeting, the BoE has bought £148bn of existing gilts currently at a rate of almost £14bn a week and also bought £152bn of newly issued gilts, thereby ensuring that the private sector did not have to increase its holdings of gilts substantially. This is allowing the government to borrow and spend; fact. Meanwhile, according to the FT, UK Chancellor Sunak is preparing to break the triple lock on state pensions as the treasury warns it could become unaffordable by 2022 due to C-19. (The triple lock ensures the state pension goes up by whichever is higher; wages, inflation or 2.5 per cent). The expected breaking of the triple lock, which was introduced by David Cameron’s coalition government in 2010, would start a big debate about whether it is affordable in the long run. This could be rather unpopular with the grey-haired Tory voters and Boris needs to restore confidence as to be honest, the Covid issue has left them wanting and ratings are tumbling. In addition, in Starmer they have a formidable foe.

—————————————————————————————————————-

Strategy:

Macro:.

Long EURGBP @.8978 added @ .8940. Stop at .8900

Long EUR @ 1.1360.. Stop at 1.1200ish. Added at 1.1285.

Long EURAUD @ 1.6260 added at 1.6500. Closed at 1.6390.

Brought to you by Maurice Pomery, Strategic Alpha Limited.

—————————————————————————————————————-

Strategic Alpha Report Disclaimer

Doo Prime endeavor to ensure the reality, adequacy, reliability and accuracy of all the information provided, but do not guarantee its accuracy and reliability. All the information, analyses, comments, statements, and/or data provided in this report is for information purposes only. Client’s use of any contents of the report as the basis for the transaction, the client shall fully aware of the risks and agreed to bear all the risks. Client shall cautiously judge the accuracy of the information. Doo Prime has no liability for any loss caused by any inaccuracy or omissions of the contents and subjective reasons of Client.

Risk Warning

This information is powered by Strategic Alpha. Any opinions, news, research, analyses, prices, other information, or links to third-party sites are provided as general market commentary and do not constitute investment advice.