Good morning.. Still nothing dents the confidence of global equity markets with another positive close on Wall St and further gains in Asian markets overnight. Clearly the sole emphasis is on central bank activity which many investors believe trumps all else (see below). But markets do not dump when the market is short and stats suggest that shorts in S&P are at the highs and we still have billions sitting in MM funds earning nothing (see below). The impact on the USD from this continued rise in stocks is beginning to do a lot of damage to the technical picture for many currency pairs… Today sees the start of the (final) talks between the UK and EU on a trade deal but hopes are not high for a conclusion and Boris is off to meet Von der Leyen later this month. Negative headlines look possible unless some serious concessions or a compromise can be found quickly as the deadline for the UK to request an extension of up to two years is the end of June. No data of note today.. EUR crosses starting to look weaker as we head into the ECB meeting..

Keep the Faith..

Details 02/06/20

The Big Question: Last round of Brexit talks start:

–

It is becoming blatantly clear that one thing and one thing alone matters for equity investors at the moment and that is the words spoken by Fed Chair Powell, when he suggested that there is “no limit to the amount of money they can print”. Economic and geopolitical risks appear to have no impact whatsoever even with 36mln Americans on Jobless benefits and riots on the streets; a global pandemic which has no vaccine is still of no concern to equity bulls and therefore we have to ask if there is nothing that can stop this bull run as long as the Fed suggests they will do whatever it takes with as much as it takes to keep markets supplied with free money. Does nothing else matter? Or, should we ask, for how long does it not matter? But I have another question that I feel has never really been answered; did we ever really recover from 2008 or did we see that can kicked down the road and are we seeing phase2 and a serious aftershock happening now. That begs the question of how long is the road? Or put it differently, are we yet to hit our “Minsky moment”? Mind you, betting against the Fed to date has brought few rewards but can this 2nd wave of economic stress so soon after the 2008 GFC, really be finally repaired? The danger here is we kick this a little further and then the roof falls in, as we are now moving to unchartered waters with few precedents with monetary policy. S&P daily below:

(The technical picture remains pretty convincing as we remain above the mid-Bollinger band and the outer bands are starting to widen marginally. Not screaming bullish but enough for some to keep hold of longs for now).

Maybe we need to focus on the things the Fed cannot fix and to be honest the list is growing. The Fed cannot fix the unemployment issue facing the US right now; it cannot fix the rioting on the streets and the potential political fall-out from that; it cannot fix the corporate margin collapses and corporate defaults; it cannot fix the psychological impact on the US consumer with job insecurity and force them to spend; it cannot fix the impact of a total breakdown of the US/China relations that may impact global growth and any recovery in trade; it also cannot fix slow growth and zero inflation by following the same policies as the BoJ; it cannot fix the fact that the US will be importing deflation and it cannot fix the global demand drought as the cheap loans they make available are simply not wanted. But hey, the banks happily take the money and stuff it in stocks, so everyone is happy for now. I am sorry but at some point the Fed may well be doing all it can but it may not be enough as the Fed cannot reach all parts of what is the make-up of the United States.

My fear is that the world is facing a twin shock here with the first wave in 2008 but the second wave may actually dwarf that. We have no idea where or when the impact from the shutdown will end or where growth and unemployment will be in a years’ time. We may recover quickly as equity investors seem to believe but listening to our clever and well-informed central banks, that seems unlikely. Governments in the US and around the world have dumped austerity and gone a massive spending spree that one would only expect during a war and this one is dwarfing that now. I have another question; why is it only now that people suggest that sovereign and corporate debt no longer matter? If so, then why did it matter in the past? As this fashionable appetite for debt spreads from the US, UK and EU, we shall see the weaker nations start to adopt a similar stance and that is where the real danger may build and become contagious. Maybe the US, holders of the reserve currency (for now) will be able to get away with this but not others.

The Fed has clearly looked back on its “success” in the aftermath of 2008, as by the end of that year, the Fed had pumped $1.3 trillion into the economy, a sum equivalent to one-third of the annual federal budget. The central bank’s traditional toolkit, involving the manipulation of short-term interest rates, had been dramatically expanded and the balance sheet ballooned. This emboldened the UK, EU and others to start QE programmes but that was while interest rates were relatively high. The impact of such schemes now with rates at zero or below seem almost negligible as was clearly proven in Japan and yet we continue to follow this BoJ template that has got them nowhere. Why? Because the central banks fear one thing more than continually weak growth and zero inflation and that is a collapsing stock market as they forced us all into this risky asset by removing all yields in savings. Collapsing asset markets can cause the “system to fail” as was almost seen in 2008 and the central banks do not want to go there again; and the scars are only just healing.

But what IF all this money sloshing around actually hits the real economy? So much money chasing a weakened supply line has the tendency to force up prices and before you know it we could be looking down the barrel of stagflation in 2021. Right now we are facing a deflationary shock but that money is out there. All the inflation is in asset markets but there is a possibility that it does not always stay there. The numbers are almost too big to comprehend (a bit like the unemployment levels in the US). During March and the first half of April, the Fed pumped more than $2 trillion into the economy, an intervention almost twice as aggressive as it delivered in the six weeks after the fall of Lehman Brothers. Meanwhile, market economists project that the central bank will buy more than $5 trillion of additional debt by the end of 2021, dwarfing its combined purchases from 2008 to 2015. Other central banks are following the same path, albeit not on the same scale. As of the end of April, the ECB was on track for $3.4 trillion of easing, and Japan and the United Kingdom had promised a combined $1.5 trillion.

Will this generate growth and inflation? Nope; not yet anyway and Japan has been at this for about 20 years now! The Fed has now even taken on moral hazard as in the past, the Fed steered clear of Main Street lending precisely because it had no wish to decide which companies deserved bailouts and which should hit the wall. That, sadly, is no longer the case and zombies wander around the corporate world of the US. It was suggested that central banks were not mandated to monetise debt but those days are gone as the sheer size of the Treasury issuance would swamp normal buyers and the US Treasury would default; can’t have that now, can we? But they key here is that maybe debt doesn’t matter while inflation is not seen and that rates stay at zero or below. But will that be the case forever with all this money stashed in markets?

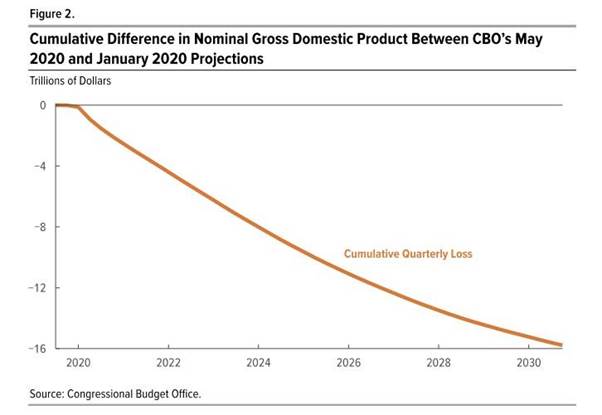

Again, what if it spills out for some unknown reason into the real economy? How do central banks deal with that as raising rates will bring the whole House of Cards down? I realise that inflation seems like a fantasy now; but it is not dead and gone forever. But as of now there are huge piles of cash sitting in money market funds and there is a suggestion that this could yet be unleashed to buy stocks if we don’t get a serious sell-off soon or solid evidence of a vaccine is found. Money-market funds have lured $1.2 trillion this year, while fund managers with $591 billion overall are holding cash at levels rarely seen in history, according to Bank of America Corp. Timing a top in equities, if indeed that is your plan, is NOT going to be easy but sometimes it just takes a spark and its gone. In its first official forecast incorporating the impact from the coronavirus shutdowns, yesterday the Congressional Budget Office said that over the 2020–2030 period, cumulative GDP will be $15.7 trillion, or 5.3%, less in nominal dollars than what the agency projected in January. Putting that number in context, the nominal GDP of the US today is $21.5 trillion, in other words over the next decade, the Coronavirus will have wiped out almost one full year of output potential from the US economy. No V-shape there then.

The CBO seem to be suggesting that it will take a decade for the impact of the coronavirus to fully fade away and for the economy to return to its pre-coronavirus normal.

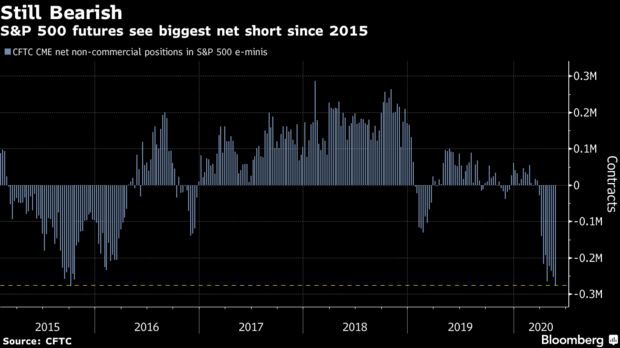

I am sure I am not the only strategist who has been frustrated by the disconnect between stocks and reality/risk; but this self-reinforcing equity rally is making a fool of those who are fundamentally negative on stocks here. Of course, this move is now hitting the USD quite hard as it had established itself as a safe haven during the early stages of the equity fall. But equity markets collapse when everyone is long and that just is not the case according to the stats. Speculators have built up the largest net short position on S&P 500 futures since late 2015, according to regulatory data. Short interest in the world’s largest exchange-traded fund — which tracks the U.S. stock benchmark — is also still hovering close to its peak in March, according to Markit data.

S&P 500 futures see biggest net short since 2015

At least I am not the only idiot losing money trying to short stocks.

Meanwhile, British and EU negotiators begin their final scheduled round of trade talks today but neither side is expecting a breakthrough. Instead hopes are being invested in a “high level” political meeting this month to thrash out a way forward between PM Johnson and Ms. Von der Leyen later this month. I have suggested a long in EURGBP which I will add to down here (GBP going through something of a squeeze in the last 2 sessions) as I think there is little hope of a breakthrough with talks and there may be some negative headlines coming. The EU is suggesting that the UK does not want a deal and the UK insist that the EU stops delaying. Something and someone is going to have to give or the UK is walking. Is Johnson prepared to take that risk? If talks fail this week and we wait for the meeting later this month, it will be a nervous wait that many investors may not wish to take.

EURGBP is holding the technical picture for now but we need to have a tight stop here below the two bases set at .8825. The break of .9000 looked impressive and impulsive but the rejection of .9050 was swift and disappointing to say the least; I expected that break to hold. This sell-off has certainly damaged the technical picture but it is worth remembering that the deadline for the UK to request an extension of up to two years is the end of June. (The techs worry me).

—————————————————————————————————————-

Strategy:

Macro:.

Long EURGBP @.8978 added @ .8940. Stop now at .8825

Brought to you by Maurice Pomery, Strategic Alpha Limited.

—————————————————————————————————————-

Strategic Alpha Report Disclaimer

Doo Prime endeavor to ensure the reality, adequacy, reliability and accuracy of all the information provided, but do not guarantee its accuracy and reliability. All the information, analyses, comments, statements, and/or data provided in this report is for information purposes only. Client’s use of any contents of the report as the basis for the transaction, the client shall fully aware of the risks and agreed to bear all the risks. Client shall cautiously judge the accuracy of the information. Doo Prime has no liability for any loss caused by any inaccuracy or omissions of the contents and subjective reasons of Client.

Risk Warning

This information is powered by Strategic Alpha. Any opinions, news, research, analyses, prices, other information, or links to third-party sites are provided as general market commentary and do not constitute investment advice.