Good Morning.. It seems the massive Pension Fund demand for equities into quarter end is real but how much has been done already? Equities are tough to trade but FX markets are not much easier with Cable flying around like a plane without a pilot. The rally nearly reached my initial target at 1.2000 and for those who took profits; well done but we are seeing some easing in the USD funding space this morning and with the stop holding yesterday, I think we could see a break higher still and on the charts, the first resistance is up at 1.2130. But in such volatile markets it is worth bagging what you can; you will always get another chance. With the Fed so active (understatement) in USTs now, I am squaring up the UST trade at little cost. Stocks look weak again this morning but this afternoon could see a bounce again; it’s not easy but one thing is clear; the numbers are rising from the virus and it would be foolhardy to ignore that, as a deep recession is coming. To my mind the really bad virus news is still to come from the US. Also from the US today we get the weekly Jobless Claims; expected to come in at 1.5mln!!!!! Quite what you do with that is any one’s guess. Keep an eye on the DXY as if we break back through 100.15, we may see the uptrend fail.

Keep the Faith..

Details 26/03/20

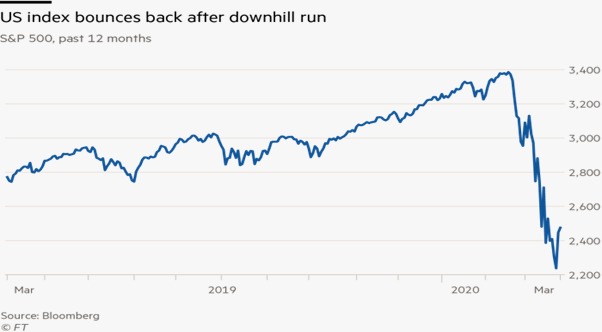

Quarter-end demand for equities from pension funds drives stock higher in the US: Central banks and governments go all-in.

I am not sure at all that the clear-out in global equities is done yet and the last two US sessions seem to be have dominated by the need from Pensions Funds to rebalance portfolios in massive numbers into quarter end. That may well continue for another day or so but stocks in Asia soon turned back down without that support. It could be another very choppy session today for stocks; both if the Pension demand is still there but certainly if it is not.

Interestingly, as stocks rallied, the VIX barely moved. In fact the VIX is now roughly where it was on Monday, largely ignoring the move in stocks.

The Nikkei lost over 5% last night before closing down 4.5% as cases rose steeply in Tokyo with HK and Shanghai marginally lower. The slide in Asia coming as the US Senate late on Wednesday passed a stimulus bill that would provide support to taxpayers and businesses hit by coronavirus to the tune of about $2trln. This virus is still spreading and without the Pension buying, I think the US would have seen stocks quite a bit lower as the news from there is far from encouraging and they seem to be on a path towards being the worst hit, while Trump is talking of getting everyone back to work. If that backfires, which it surely will, the voters may never forgive him. But it was not only stocks that had a wild ride, FX markets and especially GBP were extremely difficult to trade and hold. GBP did what it had done the day before and after making a new high just under my initial target of 1.2000, reversed nearly all the gains before a bounce back above 1.1900 yesterday.

EUR bounced on the PEPP news/rumour. If indeed true, the ECB legal decision on the PEPP is a bit of a bombshell. The 33% issuer limit will NOT apply to emergency asset purchases. The ECB will target shorter maturities (minimum 70 days!) in the hope that PEPP remains temporary. No more limits to ECB QE! ECB is going all-in and many will follow.

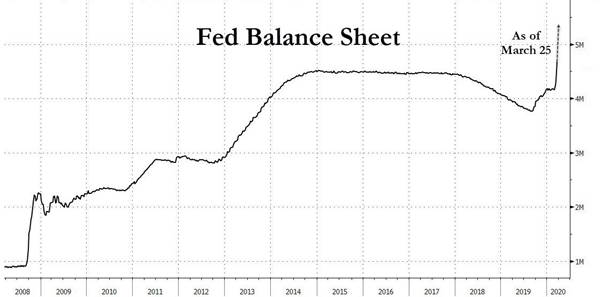

In just the past week alone, from March 19 to March 25, the Fed has purchased $587BN in securities ($375BN in TSYs, $212BN in MBS), or roughly 2.7% of the $21.4TN in US GDP.

That’s a lot; how much? This means that as of Wednesday close, when accounting for last week’s repo operations, the Fed’s balance sheet has increased by roughly $650BN, bringing it to just over $5.3 trillion, an increase of $1.2 trillion in the past two weeks, or roughly 5.6% of US GDP. Mind-boggling numbers. It is just as well the Fed is buying USTs as no one else is it seems. If we look at the Treasury securities held in custody at the Fed, it shows that the past two weeks have seen a whopping $50BN in foreign central bank sales, a 1.7% drop which was the highest in six years since Russia pulled over $100BN in TSYs from the Fed in response to US sanctions imposed over the Ukraine conflict in 2014. With all the issuance coming down the pipe, the US Treasury needs buyers; NOT sellers. What does it mean for the USD in the future if the Fed directly monetizes debt from the Treasury? Monetizing debt is not what one would expect from the reserve currency of the world!

For those who took some profits up there in Cable; well done but the stop held and we are still in this and on a more macro basis, I think the USD is still going down and that Cable could yet break above 1,2000. For many a break above 1.2000 is probably worth taking in these choppy markets and to be honest the stress in USD funding is still evident which in part was why the USD rallied yesterday but I think the Fed will keep yields down now and is fighting the stressed funding markets. BUT it is going to be choppy as there seems to be a lack of faith amongst the banks and possibly the whole USD system itself which is massively concerning; and foreign entities still appear to be hoarding dollars. I quite understand, therefore, taking any profit you can in Cable; even here at 1.1880. I think the Fed is also influencing USTs now and I am happy to jump out of the UST trade at low cost now. We need to get through month-end for a clearer picture on equities but peak virus on a global basis is still some way off. US markets totally ignored this yesterday with more bad news from the US, Spain and many others. US deaths sadly topped 1,000 with the world’s cases now topping 451,000 and more than 21,000 deaths.

Today, we get quite a bit of data but UK Retail sales this morning were for Feb. What will be more interesting is the US Weekly Jobless Claims data that is forecast to show a rise of about 1.5mln. US GDP and personal consumption are a waste of space as they are for Q4. I am not sure all the calls for a V shaped recovery are going to realised as the damage being done is pretty brutal and confidence is now extremely low in businesses and households. With regard to many businesses, we see many facing some very strong headwinds now and I am not surprised by this and mentioned it on Monday; Among the stocks hit on Thursday was Japan’s SoftBank, which dropped 8.7 per cent after rating agency Moody’s downgraded the technology group’s debt deeper into junk territory. They look very exposed here as do many other hugely leveraged multi-nationals and it should hardly come as a surprise that S&P has finally bitten the bullet and downgraded Ford debt to junk too. There is a lot more on the way.

Are we looking at a scenario where private debt is cancelled? Governments and central bankers are moving onto a war footing here and we should take note of just how concerned they are and a deep global recession looks likely now. This from Draghi last night: The challenge we face is how to act with sufficient strength and speed to prevent the recession from morphing into a prolonged depression, made deeper by a plethora of defaults leaving irreversible damage. It is already clear that the answer must involve a significant increase in public debt. The loss of income incurred by the private sector — and any debt raised to fill the gap — must eventually be absorbed, wholly or in part, on to government balance sheets. Much higher public debt levels will become a permanent feature of our economies and will be accompanied by private debt cancellation. He is, of course, correct as we have to throw everything at this and keep going. Quite how that ends, I have no idea but financial markets may never be the same again and governments and central banks are going to play a massive role in them. But as we see a massive supply shock and rising food prices, is there a danger of a period of stagflation across many parts of the global economy? Not what Central banks want to deal with.

—————————————————————————————————————-

Strategy:

Macro:.

Long Cable as of yesterday at 1.1675.. Stop at entry level…

Long US 10yr yields @ 0.835% (short USTs) Closed position.

Brought to you by Maurice Pomery, Strategic Alpha Limited.

—————————————————————————————————————-

Strategic Alpha Report Disclaimer

Doo Prime endeavor to ensure the reality, adequacy, reliability and accuracy of all the information provided, but do not guarantee its accuracy and reliability. All the information, analyses, comments, statements, and/or data provided in this report is for information purposes only. Client’s use of any contents of the report as the basis for the transaction, the client shall fully aware of the risks and agreed to bear all the risks. Client shall cautiously judge the accuracy of the information. Doo Prime has no liability for any loss caused by any inaccuracy or omissions of the contents and subjective reasons of Client.