Good morning.. S&P kept Italy’s rating in place (somehow) and as ever is a lagging indicator but this has seen BTPs push higher and the BTP/Bund spread narrow. Stocks higher yet again as the BoJ goes all in and will own the whole broken and useless JGB market. This will not create any significant growth as already witnessed in the past and yet here we go; deeper into the abyss. What really worries me is that other central banks blindly follow them. It is proven not to work!! But it seems as long as it helps asset prices then all will be fine. Oil is lower this morning and to my mind vast swathes of this industry will have to shut down. Meanwhile, the USD is lower and AUD is outperforming while EUR underperforms. This EUR underperformance may continue into the ECB meeting this week. We also have the Fed meeting and a lot of data this week and month end to consider too so it could be a choppy one. So far all that seems to matter is liquidity as bonds are so manipulated by central banks they are losing their use as a viable, forward looking indicator. Maybe oil is a better vehicle. But from the collapse of the oil industry and rising corporate defaults due to the seismic shake the world has encountered, will come the stress in the credit space; it’s just a matter of time. Until then, equity investors are happy to remain focused on central bank liquidity and this may see my stop in S&P hit.

Keep the Faith..

Details 27/04/20

Potentially a big week ahead; stocks rise in quiet markets:

–

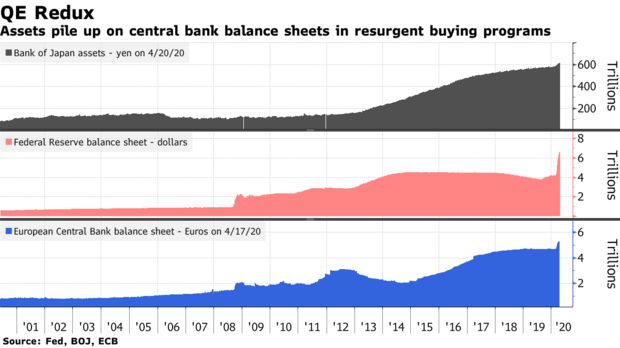

My recommendation to sell US equities is at risk and it now seems clear to me that barring some very bad news, stocks will likely keep driving higher as it is clear that shocking data is not enough to concern equity investors or that there is a danger of credit risk as defaults look likely. They are not interested in a potential risk; they will only sell if they actually see it happening. There is a danger that my stop gets hit in this environment and so anyone looking to sell simply has to wait until solid evidence is seen that things are stressing in the credit space. The other danger to the position, which looks like I was too early, is that we have 3 central bank meetings this week to consider and equity investors seem to like the fact that central banks are so concerned they may consider doing more easing or assuring us that these policies will remain in place. We started last night with the BoJ where they announced that there is now no limit to how many JGBs they can buy. That JGB market is now officially owned by the BoJ and is broken. JGB’s will no longer (and have not been for a while) an indicator for the health of the economy; it is dead to foreign investors. What worries me, is that over time, the actions of the BoJ seem to be the template for the rest of the world’s central banks. The Nikkei was up another 2.5% last night which dragged HK and Shanghai up and S&P futures; it’s all good but Abe said that he wants to start cash handouts ASAP in May (maybe not so good then). Meanwhile, the ECB is talking of buying Junk now; that will save us! One thing to note in all this, while the Fed has suggested it can now buy some ETFs and Junk, so far, they haven’t.

With central bank activity seemingly so important for stocks, one does wonder how on earth they reverse these measures if they are successful as surely that would create a massive sell-off. But that is for the future and I fear that the Fed maybe so involved in manipulating the US bond market that its importance of a forward-looking indicator is being eroded fast; just like in Japan. Bonds seem to indicate that risks are high but unfortunately, I think the yields are so low due to the Fed’s presence generally.

Regarding the Fed meeting on Wednesday, investors will be looking for any indications from Powell on how deep the Fed fears the recession will go and its outlook for recovery. He is unlikely to give a green light to those looking for policy withdrawals as the Fed will want to see the US economy back on its feet and with 26mln unemployed, that may take some time. I will be interested to hear what he says about this frightening statistic and hear how quickly he believes things can return to where they were, if indeed that is now possible. The full impact on the consumer is still an unknown going forwards. Talking of looking forwards, that is what equity investors are clearly doing but can we really see such a sudden swing back to normal after such a shockingly fast halt to global growth? Unlocking economies may be on the cards but social distancing will likely remain. Are we looking at a new normal? I just feel that pricing in things to return back to where they were is high risk but clearly many don’t.

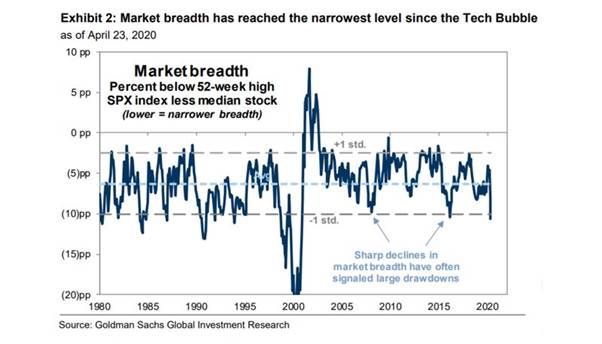

What was once dismissed as a mere “bear market rally” (often strong but ultimately doomed bounces that can occur in the middle of severe downturns) has now turned into a 23 per cent (plus) jump for global stocks. Technically, that qualifies as a new bull market and investors are scrambling for equities, especially tech names (but not banks and a few others). But the S&P is now dominated by just 5 stocks which make up 20% of the gauge’s market capitalization, exceeding the 18% level the measure reached in March 2000 and raising investor concerns about narrow market breadth. (Sharp declines in market breadth in the past have often signalled large market drawdowns).

Breadth narrowed ahead of the recessions in 1990 and 2008, in the tech bubble, and during the economic slowdowns of 2011 and 2016. Away from the top 5, less than half the members of the S&P 500 were trading above their 50-day moving average. But equity investors are seeing positive news on the virus and its peak as stats suggest we may be getting through the worst now and governments are starting to consider unlocking economies. This is great news and I do hope that we are not too early with this but we are still some way off finding a vaccine and as German shops reopened, there were no celebrations as many stayed away.

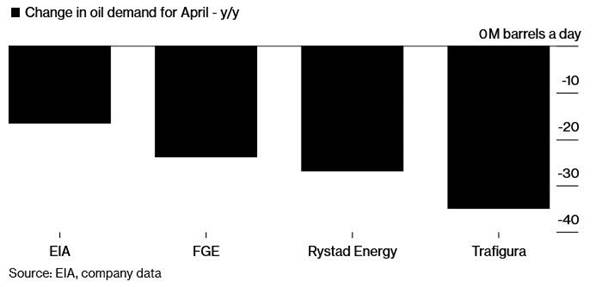

Oil is down today with Brent down 2% as fears rise of a lack of demand still and shortages in storage space and demand looks like to be an issue for a very long time still. Air travel and commuting may never be the same again. To get through this, the oil market is going to have to run close to shutting down. Stocks rallied as Trump suggested he wants to help the US oil and gas industry but I am not sure they can save them all. The fall-out could start to impact the credit space and this remains a real danger. As the recent OPEC summit so vividly demonstrated, the marginal price of oil is no longer determined by supply or cuts thereof (such as the recently announced agreement by OPEC+ for a 9.7mmb/d output cut), but rather by demand, or the lack thereof, which according to some estimate is as much as 36mmb/d lower, or roughly a third of the global oil market every day. Shale cannot live with prices like this and quite a few won’t survive (just what the Saudi’s want).

Tankers sit outside major ports full of oil no one wants.

While there is a delay between total US oil production and the rig count, it is now obvious that US production is set to collapse. Every week, another 50 million barrels of crude are going into storage, enough to fuel Germany, France, Italy, Spain, and the U.K. combined, with estimates that the world will run out of land-based storage sometime in late May or early June. Meanwhile, what’s not stored onshore, is stashed in tankers. As Bloomberg points out, the U.S. Coast Guard on Friday said there were so many tankers at anchor off California that it was keeping an eye on the situation. Maybe with bonds less of an indicator of what lies ahead, maybe we should look at oil as so far, the Fed has not started buying that.

The question here is how long the downturn lasts and so data will become more important, the longer this goes on. It is the length of time the global slowdown lasts that matters and I am not sure anyone knows how long that will be so you can see the leap of faith by equity investors. Oil markets seem to think demand will be on the floor for some time. We have GDP data from many this week and PMI data from China. This could be a significant week and month end could see distortions too. As the unemployment rises across the globe and especially in the US, payments will not be made and NPLs will spike. Payments on mortgages, auto loans and many other standing orders are not being made. Corporates are facing the same problem and cannot pay rents with profits collapsing and many may not make it. The credit space is at present supported by Fed promises but can they really bail the whole market out? There will be casualties and many businesses have been run irresponsibly; I am not sure they really should be bailed out.

It is clear that markets are engaged in a key battle between the worst evolving fundamental picture in our lifetimes on the one hand, and the largest set of liquidity injections in history. A looming $3.7 trillion deficit, a Fed balance sheets on a path to $10 trillion, zero rates as far as the eye can see and even calls for negative rates in the US with no plan or vision to ever extract ourselves from this future growth sapping venture. Record deficits, record debt, record unemployment are not a recipe for organic growth: Far from it but for now liquidity is the drug that equity investors constantly crave but at some point growth (or the lack of it) will matter. They may have done enough to head of a depression but getting back anywhere near to normal is NOT around the corner in my opinion and at some point, that will matter. Liquidity can boost asset prices but it cannot create lasting growth; quite the opposite in fact as Japan has found to its cost. Why do we want to go down that same path? I don’t get that as it clearly does not work. Maybe we need to focus away from asset markets and let them crash and have a reset. You never know it may make the world a better place in time. One step back to make two steps ahead and that is how capitalism is supposed to work and our central banks are destroying that.

—————————————————————————————————————-

Strategy:

Macro:.

Small short S&P @ 2773 added at 2809. Stop above 2880.

Long USDCAD 1.4140. Stop 1.3850ish.

Brought to you by Maurice Pomery, Strategic Alpha Limited.

—————————————————————————————————————-

Strategic Alpha Report Disclaimer

Doo Prime endeavor to ensure the reality, adequacy, reliability and accuracy of all the information provided, but do not guarantee its accuracy and reliability. All the information, analyses, comments, statements, and/or data provided in this report is for information purposes only. Client’s use of any contents of the report as the basis for the transaction, the client shall fully aware of the risks and agreed to bear all the risks. Client shall cautiously judge the accuracy of the information. Doo Prime has no liability for any loss caused by any inaccuracy or omissions of the contents and subjective reasons of Client.