Just a month ago, the biggest debate on Wall Street was simple.

When will the Federal Reserve cut rates, and by how much?

Whether it would happen was never in question.

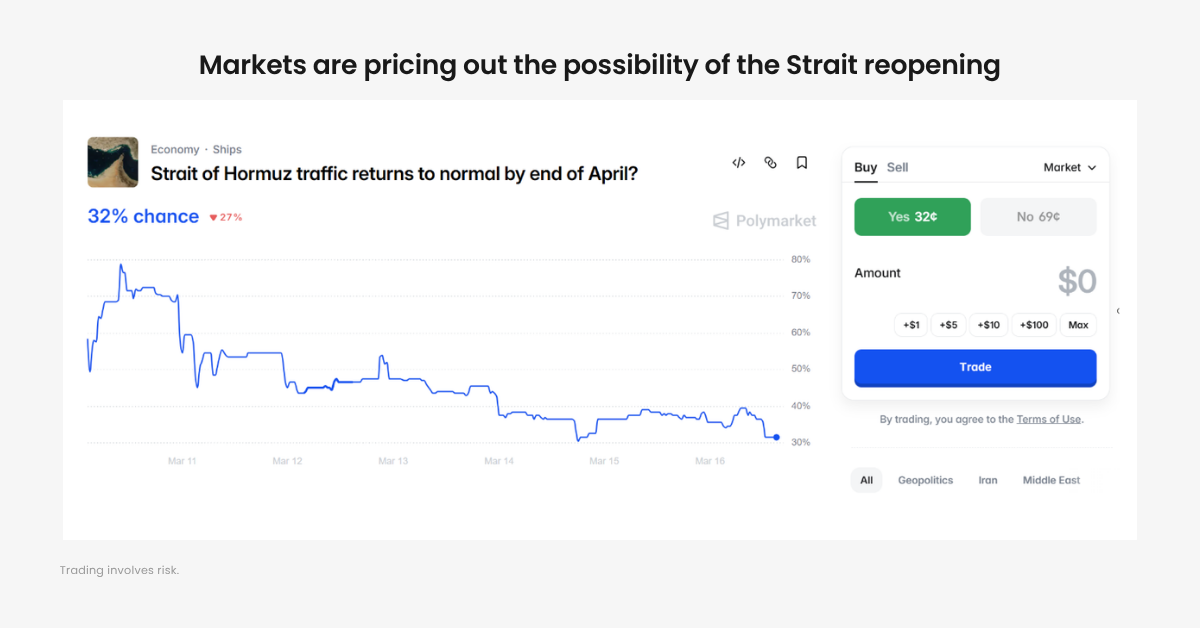

Then the Middle East conflict escalated and everything changed.

On March 16th, 2026, Brent crude opened at $106.50, breaking above the psychological $100 level with strong momentum. Markets are no longer pricing a short disruption.

They are pricing a prolonged crisis.

And that changes everything.

The Narrative Shift: From “Quick Win” to “Long War”

At the start, markets believed the conflict would be short-lived.

Sell-offs in stocks and gold were dismissed as temporary panic.

But as the war enters its third week, sentiment is shifting fast.

Markets are now asking:

- What if this conflict lasts for years?

- Is $100+ oil the new baseline?

- Will inflation return and delay rate cuts?

- Are we heading toward stagflation instead of recovery?

- And most importantly — how do we trade this environment?

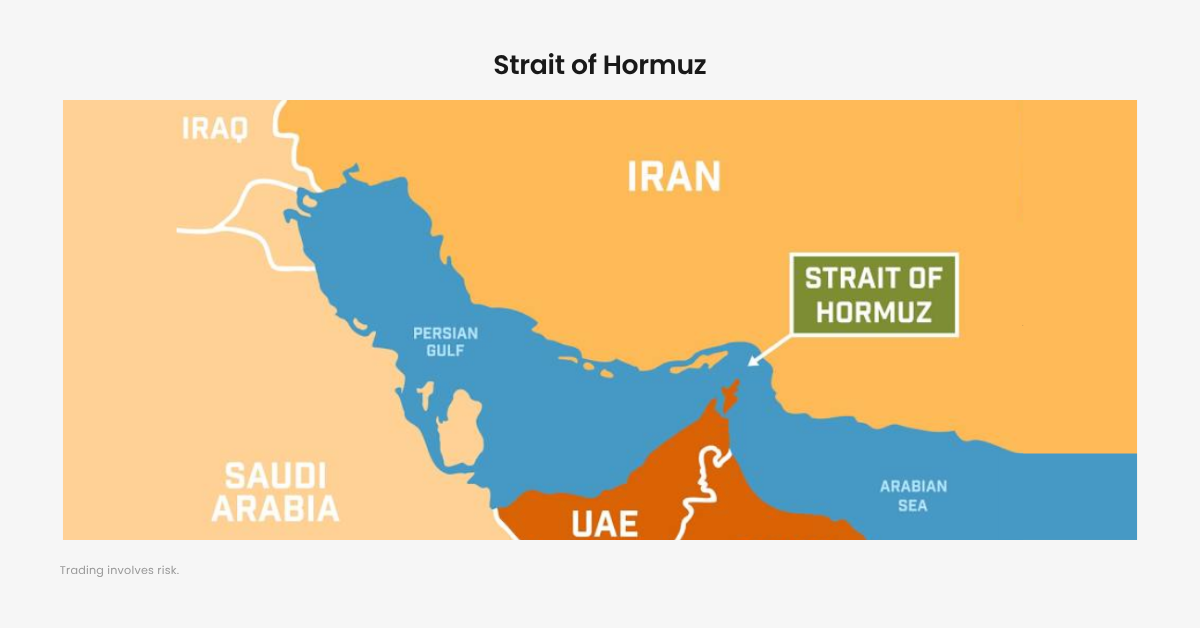

1. The Oil Shock: Why the Strait of Hormuz Matters

At the center of the crisis is the Strait of Hormuz, one of the most critical energy chokepoints in the world.

- Around 20% of global oil supply passes through it

- A significant share of global natural gas trade depends on it

Any disruption has immediate global consequences.

The International Energy Agency (IEA) has announced an emergency release of 400 million barrels from strategic reserves.

But that only covers roughly 20 days of supply disruption.

It is a temporary buffer, not a solution.

From “Short War” to “Long Conflict”

Initially, markets treated the conflict as temporary.

The early reaction in equities and gold was dismissed as emotional selling.

But as the war enters its third week, expectations are shifting.

Markets are no longer pricing a quick resolution.

They are pricing duration risk.

And Iran sits at the center of that risk.

Oil as a Strategic Weapon

This time, the pressure is not only military.

It is economic.

Inflation is the weapon.

By tightening supply through the Strait and pushing oil prices higher, Iran is applying pressure directly to the global economy.

For the United States, this exposes a structural vulnerability.

An Achilles’ heel.

Higher oil prices translate into:

- rising consumer costs

- weaker demand

- tighter financial conditions

This is pressure that spreads across the entire system.

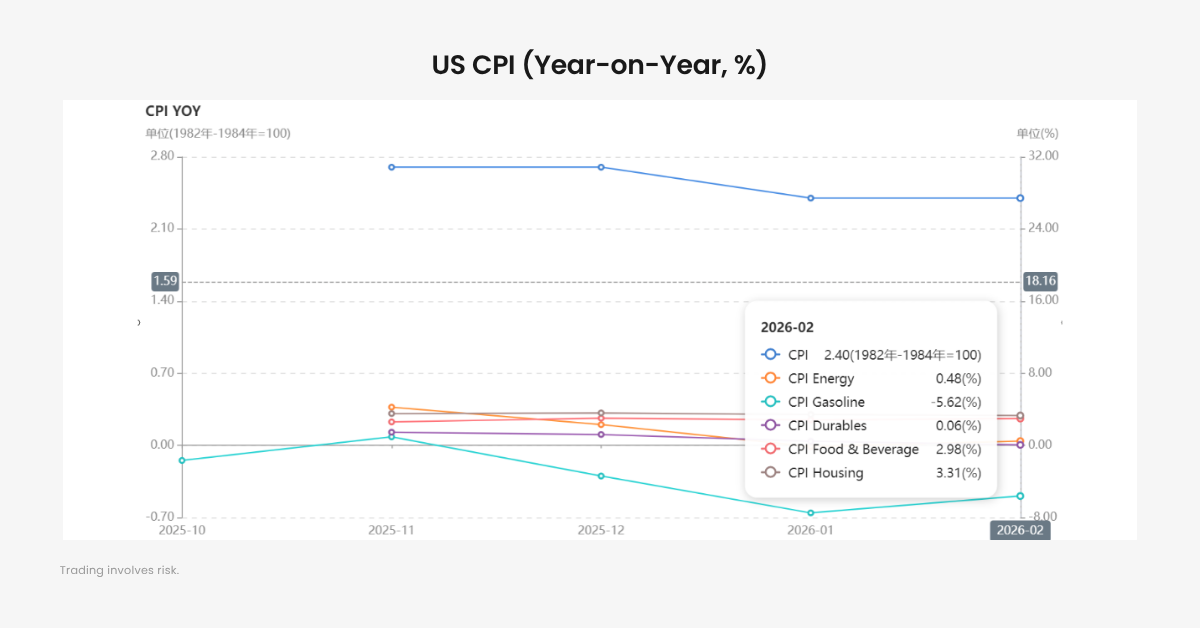

2. Inflation Risk: Is Stagflation Returning?

Before the conflict, inflation was stabilizing.

- February USCPI: 2.4%

- Driven mainly by housing and food

- Energy had not yet impacted the data

That is about to change.

How Oil Translates Into Inflation

Energy costs ripple across the entire economy:

- transportation costs rise

- production costs increase

- food prices are affected

Even agriculture is exposed.

Around one-third of global seaborne fertilizer trade passes through the Strait of Hormuz.

This is not just an oil shock.

It is a broad cost shock.

How High Could Inflation Go?

Historical data provides a guide:

- Every $10 increase in oil adds roughly 0.2% to US inflation

If oil rises:

- From $70 to $120 → inflation could reach ~3.4%

- In a prolonged conflict → oil at $150 could push inflation toward 5%

Inflation is not gone.

It is returning through energy.

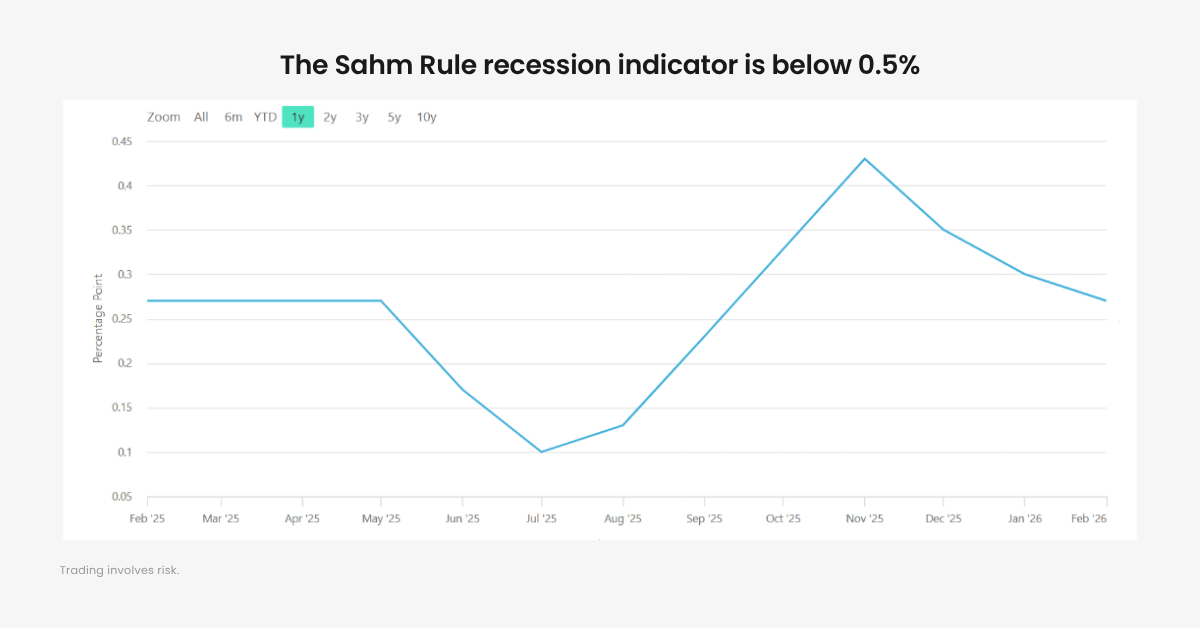

Not a Recession But a Structural Shift

At first glance, recent labor data appears weak.

But the composition matters.

Job losses are concentrated in:

- healthcare

- IT

- professional services

These sectors are being reshaped by AI and automation.

This is not a traditional recession signal.

It is a structural labor shift.

Meanwhile:

- PMI remains above 50

- The Sahm Rule indicator remains below recession thresholds

- Pre-war economic momentum was stable

The most likely outcome is not a deep recession.

It is mild stagflation:

- inflation rising

- growth slowing

- but no systemic collapse

3. Will the Fed Hike Rates Again?

The key question now is policy.

A month ago, rate cuts were certain.

Now, even rate hikes are back in the conversation.

Why Hikes Are Unlikely But Still Important

D Prime’s view remains:

A rate hike is unlikely.

But the fact that markets are discussing it again is significant.

The Fed faces multiple constraints:

1. Labor Market Fragility

AI-driven disruption is keeping employment in a delicate balance.

2. Already Restrictive Rates

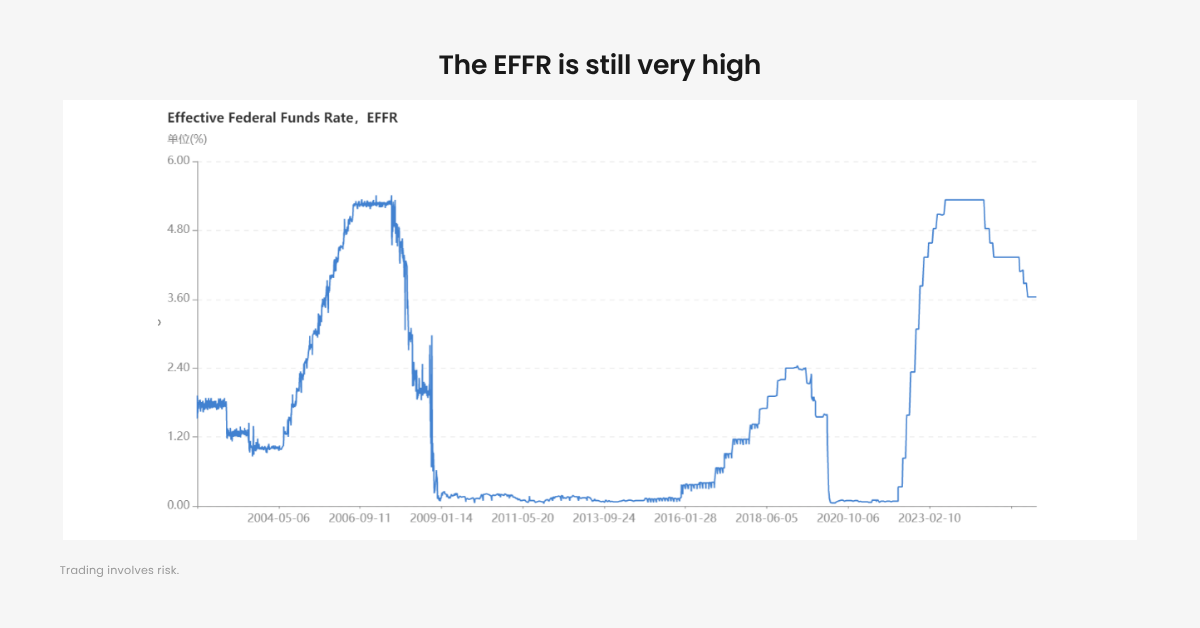

The Federal Funds Rate remains near its highest level since 2008.

3. The Debt Constraint

The US faces a major refinancing challenge:

- Around $17 trillion in Treasuries maturing

Higher rates would significantly increase borrowing costs.

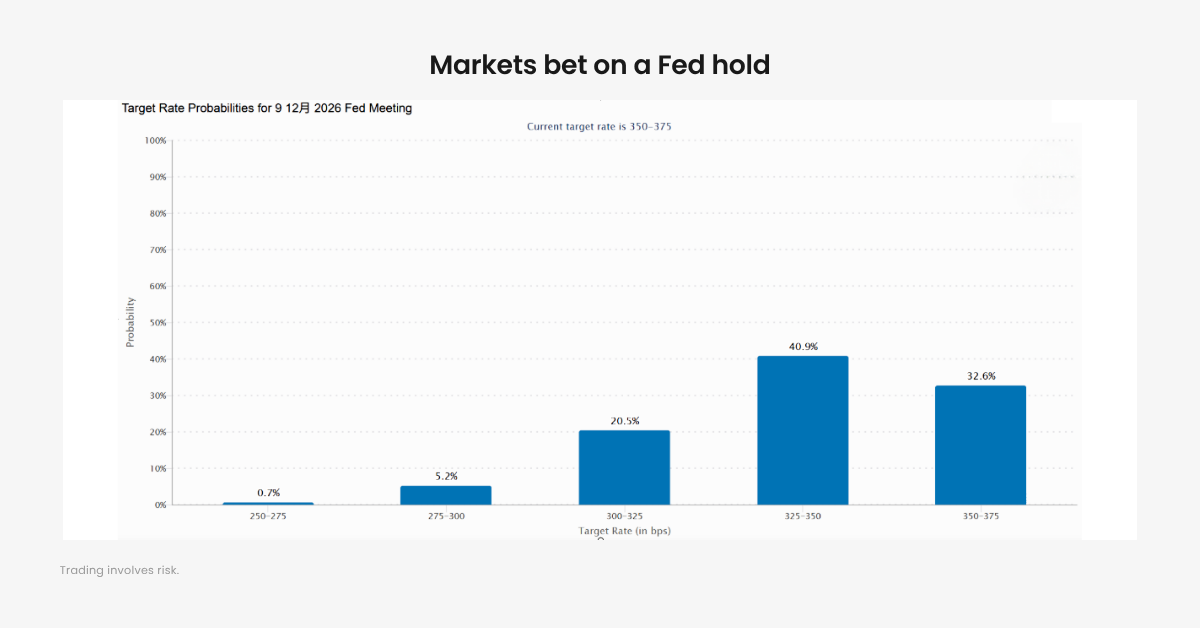

Market Expectations

CME data shows:

- A high probability of a rate hold through mid-year

- Probability of holding remains above 50% until October

- Markets still expect at least one rate cut, likely toward year-end

The shift is not just in direction.

It is in timing.

4. Trading Opportunities: What to Watch Next

Markets have already adjusted.

The expectation of a prolonged conflict is largely priced in.

That changes where opportunities lie.

Scenario 1: De-escalation

If tensions ease or the Strait is secured:

- Oil could drop sharply

- Stocks could rebound

- Gold may retrace

- Risk appetite could return

This is where the largest moves may occur.

Scenario 2: Prolonged Conflict

If the “long war” continues:

- Oil remains elevated

- Inflation stays persistent

- Rate cuts are delayed

In this case, focus shifts to:

- energy assets

- inflation-linked instruments (TIPS)

Where Markets Go From Here

The shift from rate cuts to inflation risk happened quickly.

But it is not random.

It reflects a deeper change:

Markets are no longer pricing a short disruption.

They are pricing a prolonged structural risk.

For traders, the goal is not to predict headlines.

It is to understand how capital reacts when narratives change.

Because in markets like this:

Volatility is not the biggest risk.

Misreading the cycle is.

Risk Disclosure

Trading in Securities, Futures, contracts for difference (CFDs) and other financial products carries high risks due to the rapid and unpredictable fluctuation in the value and prices of these financial instruments. This unpredictability is due to the adverse and unpredictable market movements, geopolitical events, economic data releases, and other unforeseen circumstances. You may sustain substantial losses including losses exceeding your initial investment within a short period of time.

You are strongly advised to fully understand the nature and inherent risks of trading with the respective financial instrument before engaging in any transactions with us. When you engage in transactions with D Prime, you acknowledge that you are aware of and accept these risks.

Disclaimer

This article may contain speculative statements regarding future expectations, plans, or projections based on information and assumptions currently available to D Prime. Although D Prime considers these assumptions reasonable, such statements involve risks, uncertainties, and factors beyond D Prime’s control, and actual outcomes may differ significantly.

This information contained in this blog is for general informational and educational purposes only and should not be considered as financial, investment, legal, tax or any other form of professional advice, recommendation, an offer, or an invitation to buy or sell any financial instruments. The content herein, including but not limited to data, analyses and market commentary, is presented based on internal records and/or publicly available information and may be subject to change or revision at anytime without notice and it does not consider any specific recipient’s investment objectives or financial situation. Past performance references are not reliable indicators of future performance. D Prime and its affiliates give no assurance that any views, projections, or forecasts will materialize.

D Prime and its affiliates make no representations or warranties about the accuracy or completeness or reliability of this information and disclaim any and all liability for any direct, indirect, incidental, consequential, or other losses or damages arising out of or in connection with the use of or reliance on any information contained in this article. The above information should not be used or considered as the basis for any trading decisions or as an invitation to engage in any transaction. Do not rely on this article to replace your independent judgment. You should conduct your own research and consult with an independent qualified financial advisor or professional before making any financial trading or investment decisions.

“D Prime” is a brand name of D Prime Vanuatu Limited, a company incorporated and regulated by the Vanuatu Financial Services Commission (Company Number: 700238). The availability of products and services may vary depending on jurisdiction and applicable regulatory requirements.