Magnificent 7 Earnings: Big Tech Splits Before Nvidia’s Next Test

A week after Magnificent 7 earnings, the message is clear: Big Tech is no longer trading as one simple AI basket. For traders, the opportunity is now in dispersion, follow-through, capex risk and Nvidia’s next signal.

The earnings headlines are already old.

The price action is not.

One week after the Magnificent 7 earnings rush, traders have had time to see what really mattered. The real story was not the earnings beat. It was the reaction.

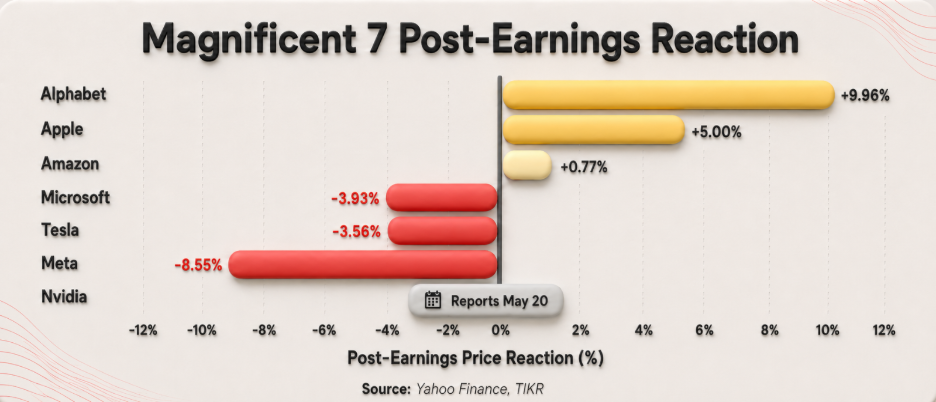

Alphabet surged. Apple was rewarded. Amazon barely moved. Microsoft fell despite strong Azure growth. Meta sold off. Tesla stayed under pressure. Nvidia has not reported yet.

The old trade was simple:

Buy Big Tech. Buy AI. Buy the dip.

That trade has changed.

Now the market is asking a harder question:

Who is actually getting paid for AI?

Quick Market Read

- Best momentum signal: Alphabet

- Best capital discipline signal: Apple

- Biggest capex concern: Meta

- Strong business, weak reaction: Microsoft

- Middle-ground setup: Amazon

- Highest narrative risk: Tesla

- Next catalyst: Nvidia earnings on May 20

- Core trading theme: Dispersion, not direction

Why Magnificent 7 Earnings Still Matter One Week Later

Most earnings recaps lose value after 24 hours.

This one still matters because follow-through is the signal.

Earnings night gives the reaction. The week after shows whether traders are still buying strength or selling good numbers.

And one week later, the verdict is clear:

Big Tech has split into leaders, laggards and wait-and-see names.

This is a dispersion trade now.

Post-Earnings Price Action: The Real Market Signal

The numbers were strong across much of Big Tech.

But the market did not reward everyone.

Source: Yahoo Finance, TIKR

| Company | One-Day Reaction | What Traders Saw |

|---|---|---|

| Alphabet | +9.96% | AI and Cloud looked like real monetization |

| Apple | +5.00% | Strong iPhone cycle and capital discipline |

| Amazon | +0.77% | AWS strength helped, but capex concerns capped the move |

| Microsoft | -3.93% | Azure growth was strong, but AI spending anxiety weighed |

| Meta | -8.55% | Higher capex guidance triggered an ROI reset |

| Tesla | -3.56% | Still the group’s most uncertain narrative |

| Nvidia | Reports May 20 | Final test for AI infrastructure demand |

The message is simple:

The market is no longer rewarding AI spending alone. It wants visible payoff.

Alphabet had the clearest AI receipts. Meta carried the loudest AI invoice. Microsoft proved that even strong Azure growth can be sold if spending worries dominate. Amazon sat between both camps: strong AWS momentum, but not enough to erase capex concerns.

This is not an “AI is dead” story.

It is an “AI is getting audited” story.

AI Receipts Beat AI Promises

Earlier in the rally, AI exposure was enough.

Now traders want evidence.

Cloud growth, margin resilience and free cash flow are being rewarded. Capex without clear revenue upside, vague long-term promises and margin pressure are being questioned.

That is the new framework:

Receipts are being bought. Invoices are being sold.

The Split: Winners, Capex Risks and Narrative Trades

Alphabet Earnings: The Clearest AI Proof

Alphabet was the cleanest winner.

The company reportedly delivered revenue of around $109.9 billion, up 22% year over year, with EPS of $5.11. Google Cloud reportedly crossed $20 billion in quarterly revenue, with growth cited around 63%.

For traders, the key was not just growth. It was monetization. Search remained resilient, Cloud accelerated, and AI looked tied to revenue.

That made Alphabet the clearest AI proof stock in the group.

Apple Earnings: Growth Without the Capex Burden

Apple was rewarded for capital discipline.

The company reportedly delivered revenue of $111.18 billion, up 17%, with EPS of $2.01. iPhone revenue reportedly rose 22%, helped by the iPhone 17 cycle.

Unlike the hyperscalers, Apple does not carry the same AI infrastructure burden. In a market worried about capex, that mattered.

Microsoft Earnings: Strong Azure, Weak Reaction

Microsoft remains a strong business, but its stock reaction mattered.

Revenue reportedly came in around USD 82.9 billion, up 18%, with EPS of USD 4.27. Azure reportedly grew around 40%.

Normally, that would be enough. This time, it was not.

Microsoft was questioned because expectations were already high and AI spending remains heavy. The market’s message was clear:

Great company. Great cloud growth. Now show the return.

Meta Earnings: The Clearest Capex Fatigue Signal

Meta was the clearest example of capex fatigue.

AI can improve ad targeting, recommendations and campaign automation. But reports that Meta raised its 2026 capex outlook to around USD 125 billion–145 billion changed the conversation.

Unlike Microsoft, Amazon and Alphabet, Meta does not have a large external cloud business that directly sells AI infrastructure to enterprise customers.

That makes the spending harder for investors to underwrite.

Amazon Earnings: Stuck in the Middle

Amazon landed in the middle.

AWS remains a major AI infrastructure platform, so any acceleration supports the broader AI story. But Amazon also needs heavy spending to meet demand.

That leaves traders with a mixed setup: AWS strength is bullish, but capex and free cash flow still matter.

Tesla Earnings: The Highest-Beta Narrative Trade

Tesla remains the hardest name to classify.

Is it an EV company facing margin pressure, or an AI, autonomy and robotics story?

The market is still debating that.

In a market demanding proof, Tesla remains the highest-beta narrative trade in the group.

Nvidia Earnings May 20: The AI Trade’s Next Test

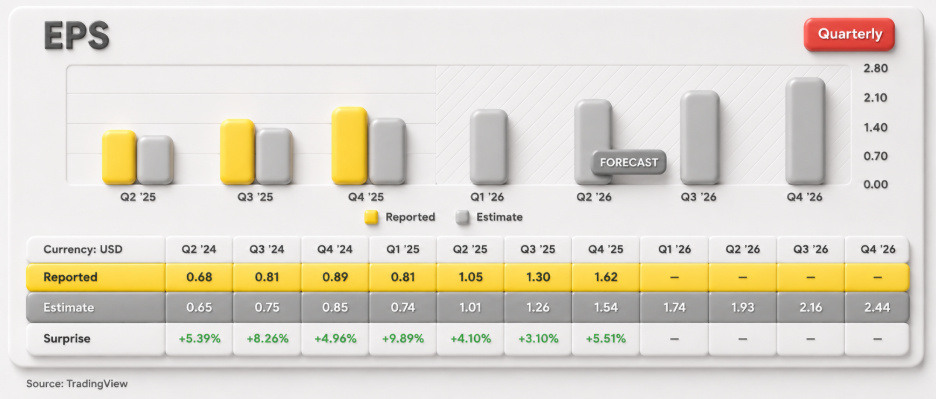

Nvidia reports on May 20, 2026.

That is the next major catalyst because the other six companies have already confirmed aggressive AI infrastructure spending. Nvidia is where that spending should show up.

Ahead of the release, analysts expect Nvidia to report USD 1.74 in EPS and USD 78.62 billion in revenue, setting a high bar for the AI infrastructure trade.

Source: TradingView

Strong data center revenue, margins and guidance would validate the AI capex cycle and support semiconductors, infrastructure stocks and Nasdaq sentiment.

A disappointment would raise a harder question:

Has the market priced AI infrastructure too far ahead?

For traders, Nvidia may decide whether this earnings season ends as:

AI cycle confirmed or AI capex questioned

Trader Framework: Dispersion, Not Direction

The old trade was Long Magnificent 7.

The new trade is Long AI monetization, avoid AI spending without proof.

| Signal | Bullish Read | Bearish Read |

|---|---|---|

| Follow-through | Winners hold gains | Winners fade quickly |

| AI capex | Spending tied to revenue | Spending rises without guidance upside |

| Cloud growth | AWS, Azure and Google Cloud accelerate | Cloud slows despite heavy capex |

| Nvidia setup | Semis stay supported into May 20 | Traders cut AI exposure before results |

If good results are bought, risk appetite is healthy.

If good results are sold, expectations may be too high.

Final Insight

The AI trade is not dead.

But the easy version is over.

Magnificent 7 earnings showed traders one thing clearly: the market is no longer buying every AI story. It is buying proof and selling promises.

Alphabet and Apple passed. Meta failed the capex test. Microsoft showed that even great growth can be sold when spending worries dominate. Amazon remains undecided. Tesla is still a narrative trade. Nvidia is the next verdict.

No more blind Big Tech basket.

For traders, the playbook is simple:

Follow the receipts. Avoid the invoices. Watch Nvidia.

Disclaimer

The information contained herein is provided for general informational and educational purposes only and does not constitute investment advice, financial advice, trading advice or any other form of professional advice, a recommendation, or an offer or solicitation to buy or sell any financial instruments or engage in any trading strategy.

Trading in leveraged products such as contracts for difference (CFDs) involves a significant risk of loss and may not be suitable for all investors. Past performance is not indicative of future results. Any references to market trends, asset performance, price levels, or forward-looking statements reflect opinions or general market commentary as at the date of publication and are subject to change without notice.

This article does not take into account any individual investor’s objectives, financial situation, or risk tolerance. Readers should conduct their own independent research and seek professional advice before making any investment or trading decisions. D Prime and its affiliates make no representations or warranties about the accuracy or completeness or reliability of this information and disclaim any and all liability for any direct, indirect, incidental, consequential, or other losses or damages arising out of or in connection with the use of or reliance on any information contained herein. The above information should not be used or considered as the basis for any trading decisions or as an invitation to engage in any transaction. Do not rely on this article to replace your independent judgment.

“D Prime” is a brand name of D Prime Vanuatu Limited, a company incorporated and regulated by the Vanuatu Financial Services Commission (Company Number: 700238). The availability of products and services may vary depending on jurisdiction and applicable regulatory requirements.